Introduction to Traceloans.com Student Loans

Thinking of taking traceloans.com student loans in 2025? Here’s the full truth—rates, risks, real reviews & safer alternatives explained.

When searching for ways to finance higher education, many U.S. students come across traceloans.com student loans. At first glance, the platform seems to offer a fast, simple way to apply online and access multiple loan options with just one form. But when it comes to borrowing for college, convenience should never come at the cost of transparency.

Why? Because student loans are not just short-term borrowing decisions—they can impact your finances for 10, 15, or even 20 years after graduation. That’s why students and parents must know whether a platform like traceloans.com is a licensed lender, or if it only acts as a loan-matching service forwarding personal information to third-party lenders.

“For a full overview of Traceloans.com across all loan types, see our Traceloans.com Review 2025.”

🔎 Key Things You Need to Know Upfront

- Traceloans.com is not verified as a direct lender — multiple independent reviews suggest it works as a lead generator.

- No clear APR ranges are published — you won’t know the actual rate until later in the process.

- No federal protections — unlike federal student loans, traceloans.com offers don’t qualify for deferment or forgiveness.

- Borrower risk factor: Sharing your personal info may lead to multiple lenders contacting you, with APRs that could be much higher than federal options.

📌 Why This Guide Matters

This article provides a complete 2025 breakdown of traceloans.com student loans, including:

- What claims the site makes,

- How the process works,

- An example repayment calculation,

- Pros & cons,

- Transparency risks,

- Safer alternatives such as federal loans and private lenders like SoFi, Sallie Mae, and Discover,

- Real user reviews from Reddit and Quora,

- Practical tips for students considering loan consolidation or refinancing.

👉 By the end, you’ll have all the information you need to decide whether traceloans.com student loans are worth considering—or if safer, regulated options are the smarter move.

Table of Contents

What Claims Traceloans.com Makes for Student Loans

On its website and across promotional content, traceloans.com student loans are often positioned as a “fast and simple” way to cover the cost of higher education. The platform highlights the idea that a student or parent can fill out one form and receive multiple loan options from different providers. While this sounds attractive, it’s important to separate what is being promised from what is actually verified.

✍️ Common Marketing Claims Found Online

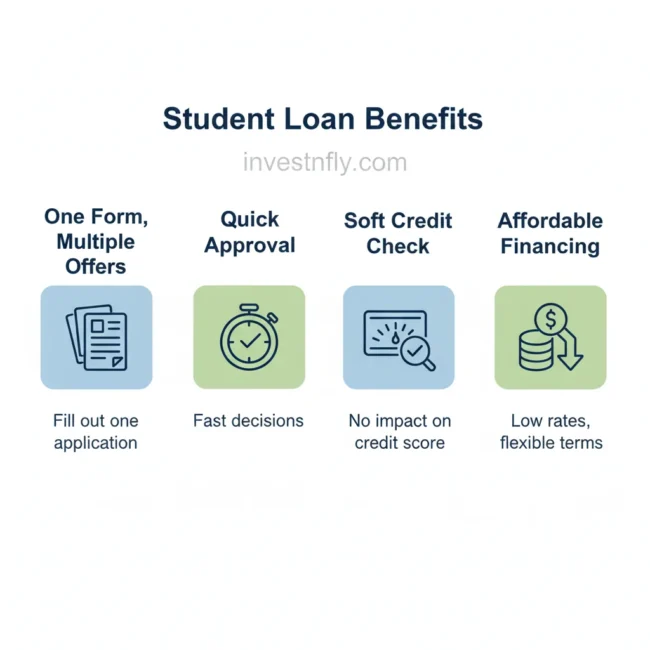

- “One form, multiple offers”

- The platform suggests that instead of applying separately with multiple lenders, you can complete a single application and instantly see various loan offers.

- “Quick approval and disbursement”

- Some reviews mention that traceloans.com promotes the possibility of faster approvals compared to traditional banks, sometimes even same-day decisions.

- “Soft credit check initially”

- The site and third-party blogs indicate that a soft inquiry may be used during prequalification, which would not affect your credit score at the early stage.

- “Affordable student financing”

- Marketing language emphasizes affordability, though no published APR ranges or fee schedules are available to confirm this.

⚠️ What’s Missing From These Claims

- No APR transparency: Unlike trusted lenders such as Sallie Mae or SoFi, traceloans.com does not publish interest ranges on its student loans.

- Licensing details not visible: There is no evidence of traceloans.com being a licensed lender listed in the NMLS Consumer Access database.

- Federal protections absent: Unlike federal loans from studentaid.gov, traceloans.com options are unlikely to qualify for deferment, income-driven repayment, or forgiveness programs.

📌 Why Students Should Be Cautious

While these claims may sound convenient, they leave major questions unanswered. Before applying, borrowers should compare offers from licensed lenders and federal programs where protections are guaranteed.

How Traceloans.com Student Loans Work

When considering traceloans.com student loans, it’s important to understand that the platform does not appear to operate as a direct lender. Instead, multiple independent reviews describe it as a loan-matching or lead generation service. That means the site collects your personal and financial information and then forwards it to third-party lenders who may reach out with offers. Knowing this flow is crucial because it affects everything from how your data is used to what repayment options are available.

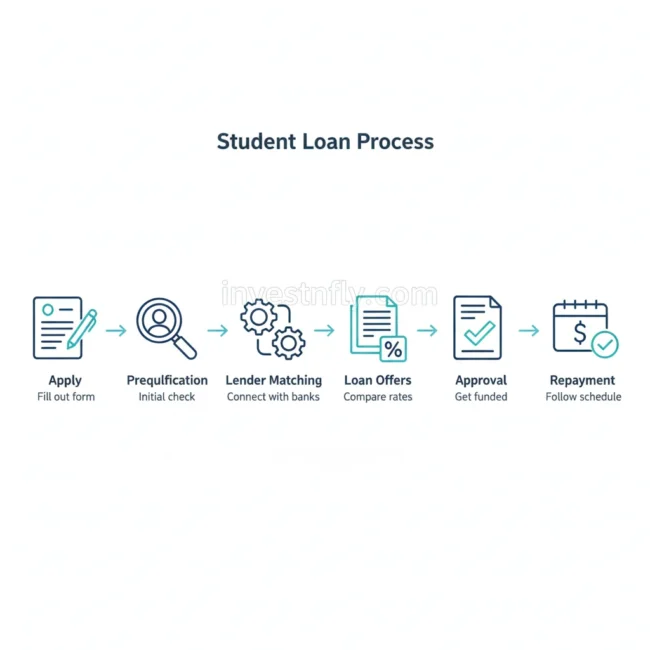

🔎 Step-by-Step Application Process

- Online Application Form

- You begin by entering basic details: name, school information, income level, and desired loan amount.

- Unlike federal applications (FAFSA), the form is short and focused on connecting you quickly with private lenders.

- Prequalification & Soft Credit Check

- According to promotional materials and some user feedback, a “soft inquiry” may be used for prequalification.

- This means your credit score won’t be immediately impacted — but remember, lenders may later perform a hard pull before final approval.

- Matching with Lenders

- Once your data is submitted, traceloans.com shares it with its network of third-party lenders.

- These lenders then decide whether to send you loan offers.

- Receiving Loan Offers

- If matched, you may receive multiple options with varying APRs, repayment terms, and fees.

- Unlike federal loans (which have standardized rates set annually by Congress), these offers depend heavily on your creditworthiness and the lender’s policies.

- Approval and Disbursement

- The lender — not traceloans.com — decides whether to approve you.

- Once approved, funds are disbursed to you or directly to your school, depending on the arrangement.

- Repayment Process

- Repayment terms vary widely. Some private lenders allow deferment while you’re in school, while others may require payments immediately.

- Traceloans.com itself does not provide repayment support — that responsibility rests with whichever lender funds your loan.

📌 Requirements to Qualify

- Credit Score: Many lenders require good credit or a cosigner, which makes traceloans.com student loans less accessible for students without established credit histories.

- Income Verification: Some lenders may ask for proof of income or future earning potential.

- School Eligibility: Not all institutions may be covered; lenders decide where their loans can be used.

⚠️ Key Repayment Concerns

- Deferment & Forbearance:

Federal student loans offer clear deferment and forbearance policies. Traceloans.com’s private lender partners may not guarantee these benefits. - Forgiveness Programs:

Federal loans can qualify for Public Service Loan Forgiveness (PSLF) and income-driven repayment plans. Private loans via traceloans.com do not qualify. - Variable vs. Fixed APR:

Without published ranges, it’s unclear if lenders provide variable or fixed rates. This creates uncertainty for long-term repayment. - Customer Support:

Borrowers will need to deal directly with the lender’s support team. Traceloans.com does not appear to manage ongoing loan servicing.

📊 Why This Matters for Students

Financing education is one of the biggest financial decisions most families make. Using a platform like traceloans.com student loans means accepting more uncertainty compared to federal loans or established private lenders like SoFi, Sallie Mae, or Discover.

- You may see multiple offers, but the lack of upfront APR disclosure makes it harder to compare real costs.

- Data privacy risks exist, since your personal details are shared with multiple third parties.

- Repayment support, deferment, or forgiveness protections are not guaranteed.

👉 Bottom line: Students should view traceloans.com as a middleman rather than a lender. While it may present quick options, it doesn’t offer the transparency or protections that federal loans and licensed private lenders provide.

Example Calculation: Student Loan Repayment Scenario

Before choosing any private student loan, it helps to see the numbers side by side. Many borrowers search for traceloans.com student loans thinking they may be affordable, but the reality can be very different when compared to federal financing. Small changes in APR and repayment terms can translate into thousands of dollars in long-term costs.

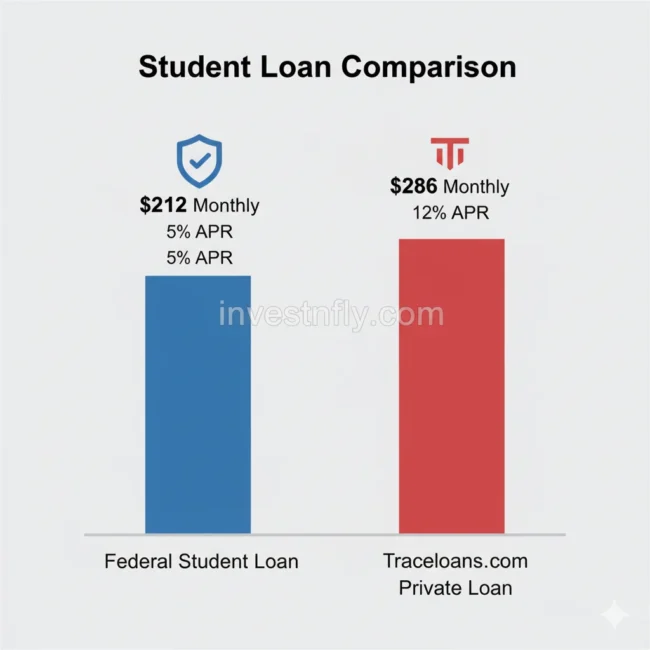

Let’s take a common example: borrowing $20,000 for college expenses with a 10-year repayment term. Below is a comparison between a standard federal direct loan and a potential private loan scenario that may come through traceloans.com student loans.

📊 Repayment Example Table

| Loan Type | Balance | APR | Term | Monthly Payment | Total Interest |

|---|---|---|---|---|---|

| Federal Direct Loan | $20,000 | 5% | 10 years | $212 | $5,440 |

| Traceloans.com (Private Match Example) | $20,000 | 12% | 10 years | $286 | $14,320 |

🔎 What the Numbers Show

- Monthly Payments

- With a federal loan, the monthly payment is around $212.

- With a 12% APR private loan, such as those linked from traceloans.com student loans, payments rise to $286.

- That’s a difference of $72 per month, which may not seem huge at first but adds up quickly.

- Total Interest Paid

- Over 10 years, the federal loan borrower pays about $5,440 in interest.

- Under the private example from traceloans.com student loans, total interest balloons to $14,320.

- That’s nearly $9,000 more over the life of the loan.

- Impact on Students

- Extra monthly costs can affect a student’s budget while still in school or just starting their career.

- Long-term, higher interest means more stress, delayed savings, and slower progress toward financial goals.

📌 Why This Matters

Federal loans not only provide lower fixed interest rates but also include deferment, forbearance, and forgiveness options that private loans typically lack. By contrast, traceloans.com student loans — if matched with high-APR lenders — can significantly increase your repayment burden.

This example shows why comparing offers upfront is so critical. Even a few percentage points in APR can mean the difference between manageable debt and long-term financial strain.

👉 “If you’re considering combining multiple debts into one, check our full Traceloans.com Debt Consolidation 2025 Guide.“

Pros & Cons of Using Traceloans.com for Student Loans

Every financial product has its strengths and weaknesses. When looking at traceloans.com student loans, it’s important to weigh the potential benefits against the risks before applying. Below is a balanced breakdown.

✅ Pros of Traceloans.com Student Loans

- One Form → Multiple Lender Matches

- Instead of applying to several private lenders separately, borrowers can complete one application and potentially receive several offers.

- Possible Fast Approvals

- Promotional content and some reviews suggest that offers may appear quickly, sometimes even the same day. This speed appeals to students needing immediate funding.

- Soft Credit Check at Prequalification

- Traceloans.com may initially use a soft credit inquiry, which doesn’t lower your score during the first stage. This makes it easier for students to explore options without immediate credit damage.

- Option for Students With Limited Choices

- Borrowers who have been denied elsewhere may still find a lender through the network connected with traceloans.com student loans.

❌ Cons of Traceloans.com Student Loans

- Not a Direct Lender

- Traceloans.com functions as a loan-matching service, not a licensed lender. This means you will work with third-party lenders, not the platform itself.

- No APR Transparency

- Unlike trusted lenders such as Sallie Mae or SoFi, the site does not publish interest rate ranges or fee structures upfront.

- Licensing Details Missing

- Independent reviews note that no verified state or federal licensing information is available in the NMLS database for traceloans.com.

- No Federal Protections

- Unlike federal student loans from studentaid.gov, private offers through traceloans.com are not eligible for income-driven repayment, deferment, or forgiveness programs.

- Potential for Higher Long-Term Costs

- Because interest rates may be higher, students could pay thousands more over time compared to federal loans.

- Data Privacy Risks

- Your personal information is shared with multiple lenders, which could lead to marketing calls and emails.

📌 Bottom Line

Traceloans.com student loans may provide convenience for students who want to see multiple private loan options with minimal upfront effort. However, the downsides — such as missing APR transparency, lack of licensing verification, and absence of federal protections — make it a high-risk option compared to federal loans or established private providers.

Borrowers should treat it as a loan-matching platform only and confirm the legitimacy of any lender they are connected with before signing a loan agreement.

Key Risks & Transparency Issues of Traceloans.com Student Loans

When dealing with private financing, transparency is everything. Unfortunately, independent reviews consistently show that traceloans.com student loans leave important questions unanswered. While the platform may connect borrowers to lenders, the lack of clarity around licensing, APRs, and federal protections creates significant risks.

📊 Risk & Transparency Table

| Risk Area | Federal Student Loans | Traceloans.com Student Loans |

|---|---|---|

| Licensing | Backed by U.S. Dept. of Education | No verified licensing details in NMLS |

| APR Disclosure | Fixed rates published annually (5–6%) | APRs not disclosed upfront |

| Forgiveness Eligibility | Eligible for PSLF & IDR forgiveness | Private loans not eligible |

| Deferment/Forbearance | Guaranteed options for hardship | Unclear, depends on partner lender |

| Data Privacy | Strictly regulated | Personal info shared with multiple lenders |

| Repayment Flexibility | Income-driven repayment available | Repayment depends on lender terms |

⚠️ Detailed Concerns

- Licensing Gaps

- Traceloans.com does not appear in the NMLS Consumer Access database.

- Without verified state or federal registration, borrowers can’t confirm oversight or protections.

- No APR Transparency

- Federal and private lenders like Sallie Mae publish interest ranges clearly.

- Traceloans.com student loans hide this information until late in the process, making cost comparisons difficult.

- Forgiveness & Federal Benefits Absent

- Federal loans can qualify for income-driven repayment (IDR) and Public Service Loan Forgiveness (PSLF).

- Private loans matched through traceloans.com do not qualify for these protections.

- Deferment and Forbearance Unclear

- Federal loans guarantee options during unemployment, medical leave, or financial hardship.

- Traceloans.com provides no clear deferment policy; terms vary by lender.

- Data Sharing Practices

- Borrower data is sent to multiple lenders. This may result in aggressive marketing or spam, with limited control for the applicant.

📌 Takeaway

While traceloans.com student loans promise convenience, they fail to provide the transparency that students and parents need when taking on long-term debt. The absence of APR ranges, missing licensing info, and no federal protections make this platform riskier than federal loans or established private lenders.

Safer Alternatives to Traceloans.com Student Loans

When financing your education, choosing a loan source with transparency and regulatory backing is essential. While traceloans.com student loans may offer quick matches, safer alternatives exist that provide clearer terms, lower rates, and stronger consumer protections.

✅ Federal Student Loans (Best First Option)

- Direct Subsidized & Unsubsidized Loans: Fixed rates set by Congress (around 5–6% for undergraduates in 2025).

- PLUS Loans: For graduate students or parents.

- Benefits:

- Income-driven repayment plans.

- Public Service Loan Forgiveness (PSLF) eligibility.

- Guaranteed deferment and forbearance.

📌 Apply at: studentaid.gov.

✅ SoFi Student Loans

- APR Range: ~4%–13%.

- Perks: Unemployment protection, career coaching, autopay discounts.

- Why Safer: Fully licensed lender with transparent terms.

✅ Sallie Mae

- APR Range: ~4%–14%.

- Perks: Cosigner release, in-school deferment, flexible repayment terms.

- Why Safer: Longstanding private student loan provider with millions of borrowers.

✅ Discover Student Loans

- APR Range: ~5%–13%.

- Perks: No origination fees, 1% cash reward for good grades, deferment available.

- Why Safer: Backed by a major financial institution with strong support services.

📊 Comparison Table: Traceloans.com vs Trusted Student Loan Providers

| Feature | Traceloans.com Student Loans | Federal Student Loans | SoFi | Sallie Mae | Discover |

|---|---|---|---|---|---|

| Licensing | No verified NMLS details | Federal government | Licensed | Licensed | Licensed |

| APR Transparency | Not disclosed upfront | Fixed ~5–6% | 4%–13% | 4%–14% | 5%–13% |

| Repayment Flexibility | Unknown, depends on partner lender | Income-driven, PSLF | Forbearance + support | Cosigner release | Flexible deferment |

| Forgiveness Eligibility | Not eligible | Eligible | Not eligible | Not eligible | Not eligible |

| Customer Support | Limited info | Federal servicers | Full support | Strong support | Strong support |

| Verdict | High-risk / lacks transparency | Safest choice | Safer private option | Safer private option | Safer private option |

📌 Takeaway

- Always exhaust federal student loans first — they offer the lowest long-term risk.

- If you need private loans, stick to licensed providers like SoFi, Sallie Mae, or Discover.

- Compared to these, traceloans.com student loans remain a high-risk option due to missing APRs, lack of licensing, and no federal protections.

👉 “Business owners exploring Traceloans.com should also review our Traceloans.com Business Loans Guide.”

Real User Reviews & Feedback on Traceloans.com Student Loans

When it comes to financial decisions, real borrower feedback is often more useful than marketing claims. Across Reddit threads, Quora discussions, and independent blog reviews, the experiences with traceloans.com student loans are mixed.

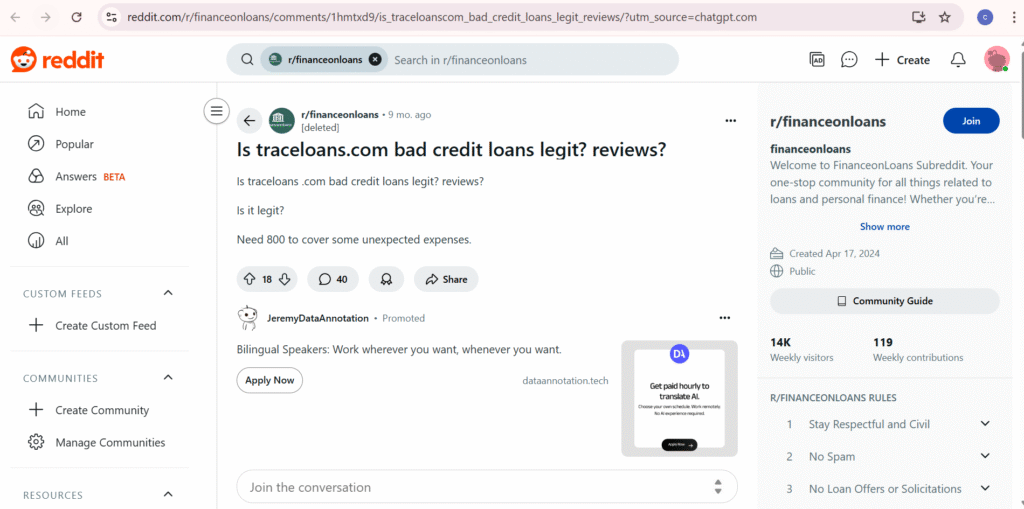

🔎 Reddit (r/financeonloans)

- Positive: Some users reported getting matched with lenders quickly and said the application was simple.

- Negative: Many complained that the APRs offered were much higher than expected (sometimes double federal rates).

- Common Concern: Fine print and fees weren’t disclosed upfront. Some users noted the platform is more of a lead generator than a direct lender.

Source: Reddit discussion

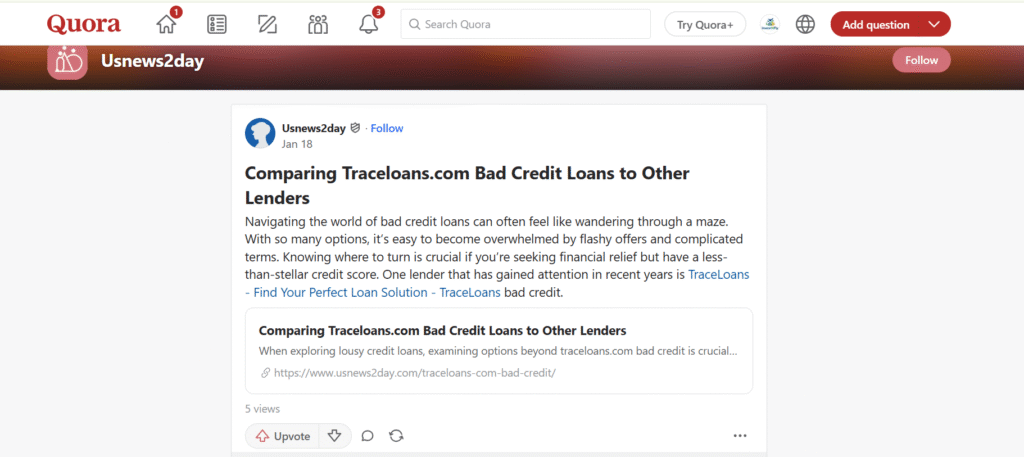

🔎 Quora

- Positive: Borrowers liked the easy-to-use interface and ability to see multiple lender options.

- Negative: Several respondents raised concerns about missing licensing details and lack of transparency around deferment and repayment protections.

- Observation: Users often compared traceloans.com unfavorably with federal loans, Sallie Mae, or SoFi.

Source: Quora: Comparing Traceloans.com to Other Lenders

🔎 Independent Blogs & Review Sites

- PartyPrott

- Describes traceloans.com as a loan-matching service.

- Notes “one form, multiple offers” claim, but warns of lack of verified licensing.

- TechScoopNow

- Highlights domain history and absence of official registration.

- Advises caution due to transparency issues.

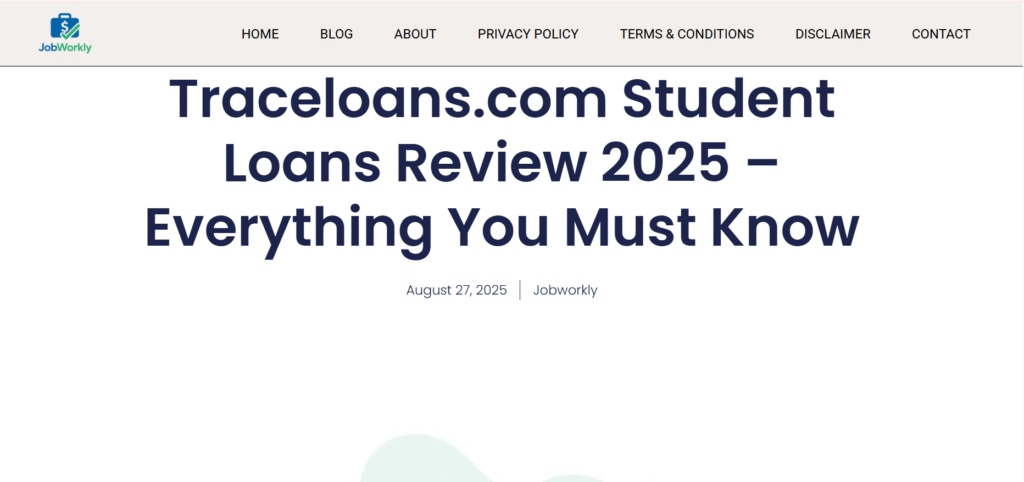

- JobWorkly

- States traceloans.com offers student loan matches, not direct lending.

- Suggests students verify lender details independently.

Sources:

“For detailed insights on how Traceloans.com handles other lending products, visit our Pillar Review 2025.”

Review Summary Table

| Platform | Positive Feedback | Negative Feedback | Verdict |

|---|---|---|---|

| Quick matches, easy application | APR higher than expected, hidden fees, acts as lead generator | Mixed but risky | |

| Quora | Simple UI, multiple options | Lack of licensing & deferment clarity | Caution advised |

| PartyPrott | One form, multiple offers | No verified licensing | Treat as aggregator |

| TechScoopNow | Explains role as loan-matcher | Missing registration & transparency | High-risk |

| JobWorkly | Covers student loan angle | Confirms not a direct lender | Verify lenders independently |

Tips & Strategies for Students Considering Consolidation or Private Loans

Managing education debt is challenging, but the right strategy can make repayment smoother and less stressful. Before committing to traceloans.com student loans or any private option, students should follow these best practices:

✅ Actionable Tips

- Always Start with Federal Aid

- Complete the FAFSA at studentaid.gov to access subsidized, unsubsidized, and PLUS loans. Federal loans almost always offer lower interest and better protections.

- Compare APRs Before Deciding

- Even a 2–3% difference in APR can add thousands in total interest. Request written offers from multiple lenders.

- Check Licensing of Lenders

- Use the NMLS Consumer Access database to confirm whether a lender connected via traceloans.com is legitimate.

- Avoid Overborrowing

- Borrow only what you truly need for tuition and essential expenses. Future repayment depends on your earning potential.

- Understand Repayment Options

- Federal loans = income-driven repayment + forgiveness eligibility.

- Private loans = limited flexibility, no forgiveness.

- Consider a Cosigner

- Many private lenders require a cosigner. A creditworthy cosigner can reduce your interest rate but also carries responsibility if you default.

- Watch Out for Fees

- Origination fees, late payment penalties, and prepayment penalties should be checked in the fine print before signing.

- Build a Repayment Plan Early

- Use loan calculators to estimate monthly payments and align them with your expected salary post-graduation.

📌 Student Checklist Before Applying

- Submit FAFSA first.

- Compare APRs from at least 3 lenders.

- Verify licensing in NMLS.

- Review deferment/forbearance policies.

- Check forgiveness eligibility.

- Confirm cosigner requirements.

- Read fine print for fees.

- Build repayment budget.

10. Frequently Asked Questions (FAQ)

1. What are traceloans.com student loans?

They are loan-matching services where borrowers are connected with third-party lenders. Traceloans.com itself is not a licensed direct lender.

2. Are traceloans.com student loans federally backed?

No. These are private loan offers, meaning they do not qualify for federal protections like income-driven repayment or forgiveness programs.

3. How do traceloans.com student loans compare with federal loans?

Federal loans usually have lower APRs (5–6%), deferment, forbearance, and forgiveness options. Traceloans.com offers vary by lender and lack federal protections.

4. Can I consolidate traceloans.com student loans later?

Yes, but only with private refinancing lenders. You cannot consolidate these into federal Direct Consolidation Loans.

5. Are there safer alternatives to traceloans.com student loans?

Yes. Safer options include federal student loans, or licensed private lenders like SoFi, Sallie Mae, and Discover.

Conclusion & Next Steps

Borrowing for education is a major financial decision that affects your future for years. While traceloans.com student loans may promise convenience, they come with uncertainties: no verified licensing, no published APR ranges, and no federal protections.

👉 If you are considering borrowing, follow this approach:

- Exhaust federal aid first (subsidized/unsubsidized loans via FAFSA).

- Compare trusted private lenders like SoFi, Sallie Mae, or Discover.

- Treat traceloans.com carefully — view it only as a loan aggregator, not a guaranteed lender.

- Always verify lenders through the NMLS database before committing.

📌 Bottom line: Traceloans.com student loans may provide quick matches, but safer alternatives exist. To protect your financial future, prioritize regulated federal or private lenders.

👉 “Borrowers should compare student loans alongside Debt Consolidation options and Business Loans to understand the full picture.”