Introduction Traceloans.com Personal Loans

Finding the right loan in 2025 can feel overwhelming. Many borrowers stumble upon traceloans.com personal loans while searching for quick cash, debt consolidation, or emergency funding. The platform looks like a shortcut—just one form and you might get multiple offers. But is it really that simple, or are there hidden risks borrowers should know before applying?

Unlike traditional banks, Traceloans.com doesn’t lend money directly. Instead, it passes your details to outside lenders who set their own interest rates and repayment rules. That means borrowers face uncertainty until after they’ve applied.

Here’s why this matters in 2025:

- ⚡ Quick matches promised → one form, many lenders.

- ❓ No upfront APR ranges → you won’t know costs until later.

- 📜 Licensing unclear → no verified NMLS details available.

- 💳 Higher potential costs → reported APRs often exceed bank rates.

- 🔒 No federal protections → unlike credit unions or government-backed loans.

👉 In this guide, we’ll break down how traceloans.com personal loans actually work, run through a $10,000 repayment example, list pros & cons, outline the biggest risks, and compare safer alternatives like SoFi, Upstart, and LendingClub.

📌 For a full overview of Traceloans.com across all loan types, start with our Traceloans.com Review 2025 – Complete Guide.

By the end, you’ll know whether Traceloans.com personal loans deserve your consideration—or if sticking with licensed lenders is the safer move.

Table of Contents

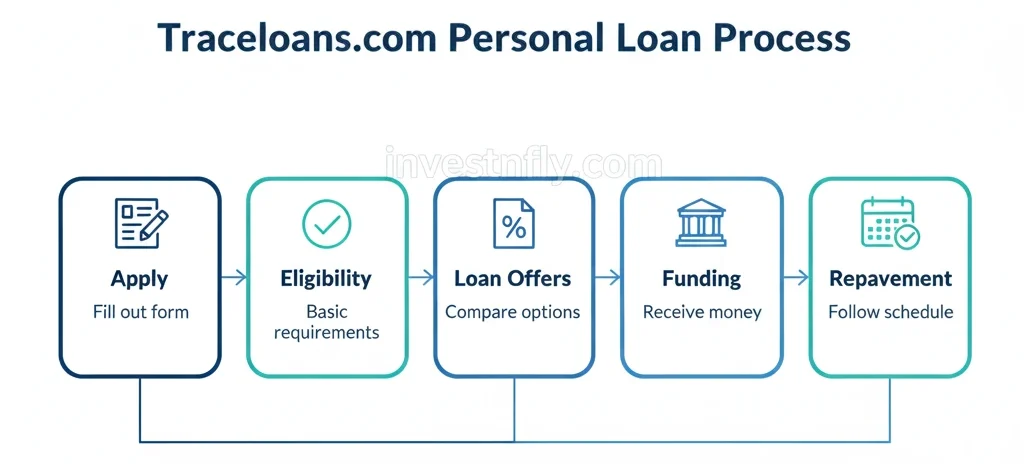

How Traceloans.com Personal Loans Work

At first glance, applying for traceloans.com personal loans looks straightforward. The site promotes “quick approvals” and “multiple offers with one form.” But since Traceloans.com is not a direct lender, the actual process works differently than most traditional banks or credit unions. Here’s how the journey typically unfolds:

🔹 Step 1: Application Form

- Borrowers start by filling out an online form on the Traceloans.com website.

- Information requested may include:

- Full name and address

- Employment details and income level

- Requested loan amount and purpose

- Estimated credit score range

- The platform claims only a soft credit inquiry at this stage, meaning your credit score should not drop just for applying.

🔹 Step 2: Eligibility Check

- Using your details, Traceloans.com forwards your application to its network of partner lenders.

- There is no published list of these lenders, which means borrowers don’t know in advance who might receive their information.

- Each lender sets its own rules for approval. For example:

- Minimum credit score requirements

- Income-to-debt ratio checks

- State-by-state licensing and lending limits

🔹 Step 3: Loan Offers

- If eligible, borrowers may receive multiple offers.

- Loan terms vary:

- APR could range widely (some users report over 20%).

- Loan amounts depend on creditworthiness.

- Repayment terms typically range from 12–60 months.

- Important: Unlike SoFi or banks, Traceloans.com does not publish an APR range upfront, so costs remain unclear until lenders respond.

🔹 Step 4: Acceptance & Funding

- Borrowers select one offer and proceed directly with that lender.

- Funding time varies from same-day approval to several business days.

- At this point, a hard credit check is usually performed, which impacts your score temporarily.

🔹 Step 5: Repayment

- Repayment is entirely controlled by the lender.

- Monthly payments depend on APR, fees, and loan term.

- Unlike federal loan programs, there are no guaranteed deferment, forbearance, or forgiveness options.

📌 Key Takeaway:

The application process for traceloans.com personal loans is simple on the surface but hides critical gaps. Borrowers cannot confirm licensing, APR ranges, or lender transparency until after applying—making it a high-risk choice compared to regulated banks or credit unions.

The steps above describe how traceloans.com personal loans appear to work based on publicly available information from the website and user reports across forums like Reddit and third-party reviews. Traceloans.com itself does not publish detailed licensing or APR ranges, and processes may vary depending on the lender you are matched with.

👉 Important: This article is for educational purposes only. We do not endorse or guarantee Traceloans.com as a legitimate or safe lending platform. Always verify lender licensing through trusted resources such as the NMLS Consumer Access database or the Consumer Financial Protection Bureau.

Example Calculation: $10,000 Personal Loan

Before choosing any private loan, it’s important to understand how much you’ll actually pay back. With traceloans.com personal loans, costs depend entirely on the third-party lender you are matched with. To make things clear, let’s compare a standard bank loan with an example match through Traceloans.com.

📊 Repayment Scenario – $10,000 Loan (36 months)

| Loan Type | Loan Amount | APR | Term | Monthly Payment | Total Interest | Total Paid |

|---|---|---|---|---|---|---|

| Bank / Credit Union | $10,000 | 8% | 36 months | $313 | $1,280 | $11,280 |

| Traceloans.com Example Match | $10,000 | 24% | 36 months | $389 | $4,004 | $14,004 |

🔎 What This Means for Borrowers

- At a bank/credit union rate of 8% APR, you’d pay about $1,280 in interest over three years.

- At a 24% APR (as some borrowers reported when using Traceloans.com), interest balloons to $4,004—almost 3x more.

- The monthly payment difference may seem small ($313 vs $389), but over 36 months, that adds up to $2,724 more out of your pocket.

⚠️ Why This Matters

Borrowers often focus on just the monthly payment. But even a few percentage points in APR can mean thousands of dollars more in total interest. That’s why it’s critical to compare lenders before accepting any offer from Traceloans.com.

📌 Tip: Always use a loan calculator before signing an agreement. You can try the free Loan Calculator or check with your credit union for transparent estimates.

Pros & Cons of Traceloans.com Personal Loans

Before you click “apply,” it helps to see the tradeoffs side-by-side. Below is a balanced look at the main advantages and disadvantages of using traceloans.com personal loans—based on how the platform advertises itself and real user reports from forums and review sites.

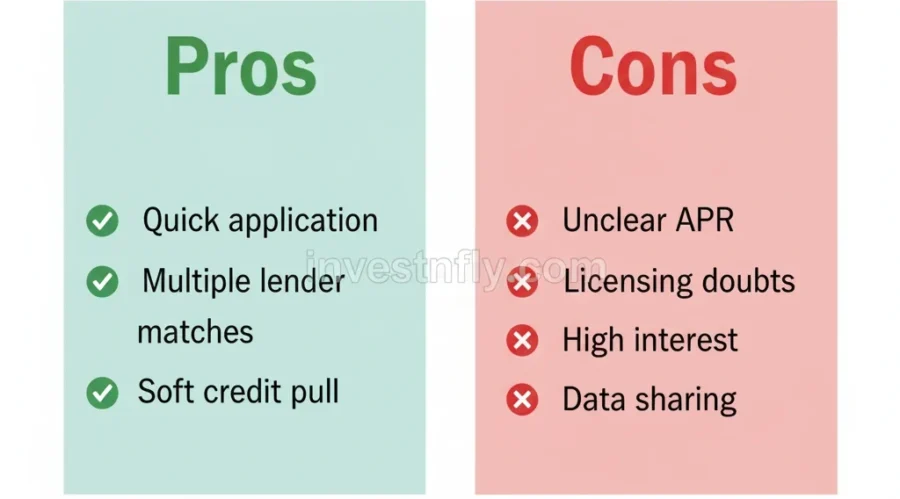

✅ Pros (Why some borrowers choose Traceloans.com)

- Single form, multiple matches. Instead of applying separately to several lenders, you fill one application and may receive multiple offers—helpful when time is short.

- Soft prequalification. The platform reportedly uses a soft credit check for initial matching, so your score may not take a hit on first lookups.

- Fast lead generation. Borrowers who need quick funding sometimes get matched and approved faster than traditional bank workflows.

- Access for thin-credit borrowers. Some applicants who are rejected by banks still receive offers from alternative lenders in the network.

- Convenience & comparison at a glance. For a shopper who wants wholesale exposure to lender options, Traceloans.com can be a time-saver.

❌ Cons (Why many experts recommend caution)

- Not a direct lender. Traceloans.com forwards your information to third-party lenders—it does not underwrite or service loans directly. That means you don’t contract with Traceloans.com; you contract with the lender who responds.

- APR transparency is limited. The site does not publish APR ranges or typical fee schedules up front, so you may only learn the real cost after offers arrive. That makes apples-to-apples comparisons difficult.

- Licensing & oversight unclear. There’s no clear public listing of Traceloans.com as a licensed lender in NMLS; borrowers should verify any lender partner independently.

- Potentially high interest & fees. User reports and some matched offers suggest APRs can be substantially higher than bank or credit union rates (see $10,000 example earlier).

- Data sharing / marketing risk. Your application details are shared with multiple partners—expect outreach from lenders and marketing affiliates.

- No federal protections. These private loans do not qualify for federal deferment, income-driven repayment, or forgiveness programs.

Quick Pros/Cons Snapshot

| Pros | Cons |

|---|---|

| One form → multiple lender matches | APRs not disclosed upfront |

| Soft prequalification | Not a direct lender (third-party loans) |

| Faster matches for urgent needs | Licensing and oversight unclear |

| Options for thin-credit borrowers | Data shared with multiple parties |

Practical takeaway

traceloans.com personal loans can be useful if you need fast exposure to multiple private lenders and you understand the risks. But because APR, licensing, and repayment protections are unclear until offers appear, most U.S. borrowers will be safer comparing licensed providers (banks, credit unions, SoFi, LendingClub) first. If you proceed, verify each lender’s licensing via NMLS Consumer Access and read the full loan estimate before accepting any offer.

👉 For context on consolidation and other loan types, see our full review at Traceloans.com Review 2025 – Complete Guide.

Key Risks & Transparency Issues

Borrowers considering traceloans.com personal loans should carefully weigh the potential risks. While the platform promotes speed and convenience, important details are missing or unclear. Below are the main concerns raised by financial experts and user reports:

1. Licensing & Oversight

- No verified listing of Traceloans.com as a licensed lender in the NMLS Consumer Access database.

- Without clear licensing, borrowers can’t confirm if matched lenders follow state/federal lending laws.

- This increases the chance of being connected with high-cost or unregulated lenders.

2. APR & Fee Transparency

- Unlike banks and credit unions, Traceloans.com does not publish typical APR ranges or fee structures upfront.

- Borrowers may only learn the true costs after submitting personal details.

- User reports mention APRs well above 20%–30%, which can mean thousands more in interest.

3. Repayment Flexibility

- Federal loan programs allow deferment, income-based repayment, or forgiveness.

- With Traceloans.com, repayment options depend entirely on the lender you’re matched with.

- Some lenders may offer limited flexibility, but there’s no guarantee.

4. Data Sharing Concerns

- Traceloans.com works as a lead generator, not a direct lender.

- Your personal details (income, credit score, contact info) may be shared with multiple lenders or affiliates.

- This can result in unwanted calls, emails, or marketing messages.

5. Unverified User Protections

- No published terms about borrower protection in cases of fraud, errors, or disputes.

- Borrowers have little recourse if terms are misleading or if a matched lender acts unfairly.

⚠️ Disclaimer:

The risks described above are based on publicly available information from the Traceloans.com website, third-party reviews, and borrower discussions on forums like Reddit. We do not endorse or guarantee Traceloans.com as a safe platform. This content is for educational purposes only. Always verify lender licensing directly through trusted resources such as the NMLS Consumer Access and consult the Consumer Financial Protection Bureau (CFPB) before applying for any loan.

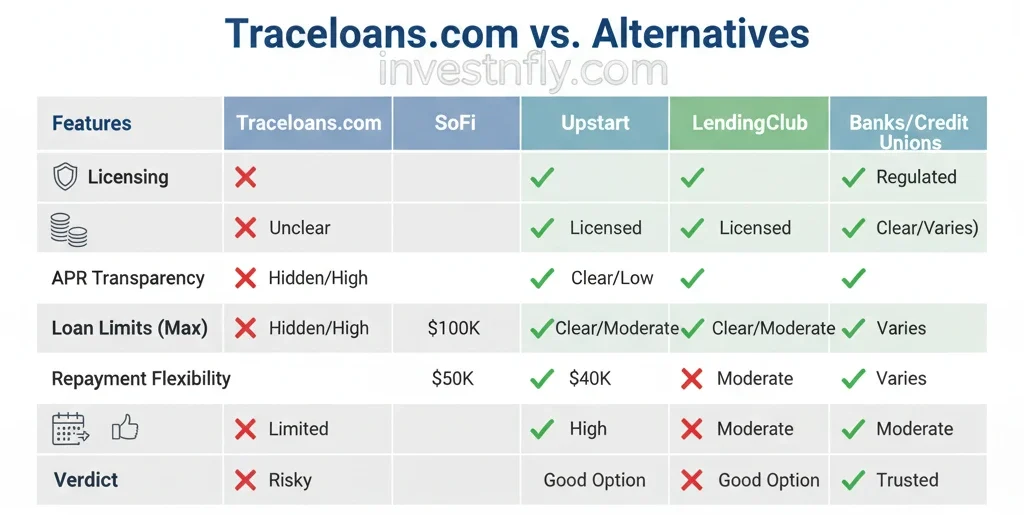

Safer Alternatives to Traceloans.com Personal Loans

For most borrowers, licensed lenders and established financial institutions are far safer than unverified platforms. Below are some of the best-known alternatives to traceloans.com personal loans in 2025, each with clear APR ranges, borrower protections, and transparent terms.

1. SoFi Personal Loans

- APR Range: ~8%–23% (depending on credit score).

- Loan Amounts: $5,000–$100,000.

- Unique Perks: No origination fees, unemployment protection, and career coaching.

- Why Safer: SoFi is a licensed lender, regulated in all states where it operates.

2. Upstart

- APR Range: ~7.8%–35.99%.

- Loan Amounts: $1,000–$50,000.

- Unique Perks: Uses AI-based credit decisioning (can approve fair-credit borrowers).

- Why Safer: Transparent APR and fee disclosure upfront; CFPB-regulated practices.

3. LendingClub

- APR Range: ~9%–35.99%.

- Loan Amounts: $1,000–$40,000.

- Unique Perks: Joint applications allowed, which helps couples or co-borrowers.

- Why Safer: Established since 2007, registered and regulated in the U.S.

4. Credit Unions & Banks (e.g., Regions Bank, Navy Federal Credit Union)

- APR Range: ~6%–18% (often lower for members).

- Loan Amounts: $500–$50,000+.

- Unique Perks: Member-focused benefits, lower fees, and face-to-face support.

- Why Safer: Federally insured institutions, strong consumer protections.

📊 Comparison Table – Traceloans.com vs Safer Alternatives

| Provider | Licensing | APR Transparency | Loan Limits | Repayment Flexibility | Verdict |

|---|---|---|---|---|---|

| Traceloans.com | ❌ No verified NMLS | ❌ Not published upfront | Unknown | Depends on matched lender | ⚠️ High-risk / unclear |

| SoFi | ✅ Licensed nationwide | ✅ Clear APR (8%–23%) | $5k–$100k | ✅ Forbearance & protections | 👍 Safer choice |

| Upstart | ✅ Licensed / CFPB-regulated | ✅ APR upfront (7.8%–35.99%) | $1k–$50k | Standard options | 👍 Transparent, fair-credit friendly |

| LendingClub | ✅ Licensed U.S. lender | ✅ APR upfront (9%–35.99%) | $1k–$40k | Joint applications allowed | 👍 Reliable for mid-credit |

| Credit Unions / Banks | ✅ Federally insured | ✅ Published ranges (6%–18%) | $500–$50k+ | ✅ Member benefits, deferment possible | 🥇 Safest overall |

💡 Key Takeaway

While traceloans.com personal loans may look convenient, safer alternatives like SoFi, Upstart, LendingClub, or your local credit union provide transparent APRs, borrower protections, and licensed lending practices. These options help you avoid hidden fees and reduce the risk of falling into high-cost debt traps.

👉 Explore safer personal loan options via Experian’s Personal Loan Guide or CFPB Loan Resources.

Practical Tips & Strategies for Borrowers

Choosing the right personal loan can save you thousands of dollars over time. Since traceloans.com personal loans involve third-party lenders with unclear terms, it’s especially important to approach with a strategy. Here’s a step-by-step checklist to guide your decision.

✅ Step 1: Check Your Credit First

- Get your free credit report from AnnualCreditReport.com.

- Use tools from Experian or Credit Karma to know your score.

- A higher score (700+) often qualifies you for lower APR loans from banks or SoFi.

✅ Step 2: Compare APR Ranges Before Applying

- Only consider lenders who publish transparent APR ranges upfront.

- Avoid applying blindly on platforms like Traceloans.com without knowing the potential costs.

- Use loan calculators (like the one on this page) to simulate monthly payments.

✅ Step 3: Verify Licensing

- Search lenders on the NMLS Consumer Access database.

- Never sign with a lender who isn’t licensed in your state.

✅ Step 4: Calculate the Total Cost, Not Just Monthly Payment

- Borrowers often focus on the monthly installment.

- Instead, look at total repayment (principal + interest + fees).

- Example: a $10,000 loan at 24% APR can cost nearly $3,000 more than at 8% APR.

✅ Step 5: Check Repayment Flexibility

- Ask about deferment, early payoff penalties, or forbearance policies.

- Credit unions and SoFi often allow flexibility, while lead generators may not.

✅ Step 6: Protect Your Personal Data

- Avoid submitting sensitive info (SSN, income) unless the lender is verified.

- Create a dedicated email for loan applications to filter marketing spam.

📌 Quick Borrower Checklist

- Pull your credit report

- Compare APR ranges side by side

- Verify lender licensing on NMLS

- Calculate total repayment costs

- Confirm repayment flexibility

- Protect your data & avoid spam

💡 Key Takeaway:

A little homework upfront can save years of financial stress. If you’re considering traceloans.com personal loans, use these steps to minimize risks and always compare with licensed alternatives first.

Frequently Asked Questions (FAQs)

1. Are traceloans.com personal loans legitimate?

Traceloans.com is not a direct lender; it functions as a lead generator that passes borrower information to outside lenders. Because the site does not publish verified licensing or APR ranges, it is unclear how safe or consistent the offers are. Borrowers should verify any lender they are matched with using the NMLS Consumer Access database.

2. What APR can I expect with traceloans.com personal loans?

Unlike licensed lenders such as SoFi or LendingClub, Traceloans.com does not disclose typical APR ranges upfront. User reports suggest APRs can be significantly higher than bank or credit union loans. Always compare offers with transparent lenders before accepting.

3. How do traceloans.com personal loans work?

Borrowers complete an online form, which is shared with Traceloans.com’s partner lenders. If eligible, offers are returned with different APRs, loan limits, and terms. Repayment is made directly to the matched lender—not to Traceloans.com.

4. Do traceloans.com personal loans affect my credit score?

Submitting the initial application may result in a soft credit inquiry, which should not affect your score. However, once you accept an offer, the lender will typically perform a hard credit check, which can temporarily lower your credit score.

5. Can I consolidate debt using traceloans.com personal loans?

Yes, some borrowers may use loan offers from Traceloans.com lenders to consolidate debt. However, without clear APR and licensing details, the total cost could be much higher than consolidation through a credit union or bank. See our Traceloans.com Debt Consolidation Guide for safer strategies.

6. What are safer alternatives to traceloans.com personal loans?

Safer, licensed alternatives include SoFi, Upstart, LendingClub, and federally insured credit unions. These lenders publish APR ranges, are regulated, and offer stronger borrower protections.

7. Should I apply for traceloans.com personal loans in 2025?

It depends on your situation. If you have fair to good credit, you may qualify for safer options with lower APRs elsewhere. traceloans.com personal loans can expose you to unverified lenders, so apply cautiously and only after comparing trusted providers.

Before You Apply: Key Takeaways & Next Steps

Applying for traceloans.com personal loans may feel like a shortcut to quick cash, but the lack of transparent APR ranges, licensing details, and repayment protections makes it a high-risk choice compared to established lenders. The platform acts as a loan-matching service, not a direct lender—meaning the terms you receive depend entirely on outside partners.

Here are the key lessons from our review:

- ✔️ Transparency matters. Without clear APR disclosures, you may end up paying thousands more in interest.

- ✔️ Licensing is non-negotiable. Always confirm a lender’s credentials in the NMLS Consumer Access.

- ✔️ Alternatives are safer. SoFi, Upstart, LendingClub, and credit unions offer transparent APRs and stronger borrower protections.

- ✔️ Preparation saves money. Checking your credit score, calculating repayment scenarios, and comparing multiple offers reduces your risk.

👉 Next Step: If you’re considering a personal loan in 2025, start by comparing safe, licensed providers with transparent terms. Use our loan calculator on this page to estimate monthly payments and visit our Traceloans.com Review 2025 – Complete Guide for a broader look at all loan types before making a decision.

💡 Bottom line: Borrowing money is a long-term commitment. Choose lenders that are clear, regulated, and supportive—your future finances will thank you.