Introduction to Credit Union Business Credit Cards

Running a business in the USA means constantly balancing costs, managing cash flow, and finding financial tools that support growth. While big banks dominate the business credit card market, many small and mid-sized businesses are discovering the unique advantages of credit union business credit cards. These cards often come with lower interest rates, fewer hidden fees, and a more personalized service compared to traditional banks.

Unlike large financial institutions that prioritize profit margins, credit unions operate as member-owned cooperatives. This means that when you join a credit union, you’re not just another account number—you’re part of a community that reinvests profits back into members through better rates and benefits. For business owners, this translates into access to affordable financing options, rewards programs tailored for everyday expenses, and financial partners who actually understand local challenges.

In this article, we’ll explore what credit union business credit cards are, why they may be better than bank-issued cards, and the top options to consider in 2025. We’ll also provide real examples, a comparison table, and helpful resources to guide you through choosing the right card for your business needs.

What is a Credit Union Business Credit Card?

A credit union business credit card is a financial product issued by a credit union specifically for business owners. Like any other business credit card, it allows you to separate business expenses from personal ones, build business credit history, and take advantage of features like cash-back rewards or travel points.

The key difference lies in who issues the card. Credit unions are not-for-profit organizations owned by their members. This structure allows them to offer:

- Lower Annual Percentage Rates (APR) compared to banks

- Fewer fees such as annual fees or foreign transaction charges

- Flexible lending terms for small and medium-sized businesses

- Personalized approval processes (credit unions may consider factors beyond just credit score)

For example, a small business owner in Texas who joins a local credit union may get approved for a business credit card even if their business is less than two years old. Traditional banks might decline the same application due to stricter underwriting rules.

Another important benefit is community reinvestment. Profits made by the credit union go back into offering better rates for loans and credit cards, not into shareholder dividends. This makes credit union cards particularly appealing for startups and entrepreneurs looking for affordable financing.

In short, a credit union business credit card is not just about borrowing—it’s about building a relationship with a financial partner that grows with your business.

Top 3 Index Funds in USA 2025 | Grow to $1M with Investnfly

Why Choose a Credit Union for Business Credit Cards?

There are several reasons why many entrepreneurs are turning to credit unions instead of traditional banks for their business credit card needs.

1. Lower Interest Rates and Fees

Because credit unions don’t operate for profit, they can pass savings directly to members. A business credit card at a bank might carry a 20–25% APR, while a credit union alternative could offer something closer to 12–15%. Over time, this difference can save a business thousands of dollars in interest.

2. Personalized Approval Process

Big banks usually rely solely on rigid algorithms and FICO scores. Credit unions, on the other hand, often consider the overall relationship and business potential. This means even businesses with limited credit history may qualify.

3. Member-Focused Rewards Programs

While banks may push generic rewards, credit unions often design reward categories that are relevant to small businesses—such as office supplies, fuel, or travel. For example, PenFed Credit Union’s business card offers extra cash-back on vehicle expenses, which is perfect for businesses that rely on fleets or regular travel.

4. Community Connection

Many business owners prefer working with a local credit union where decision-makers are accessible. This community-based approach builds trust and creates stronger financial partnerships.

5. Lower Risk of “Gotcha” Fees

Hidden charges like balance transfer fees, excessive late fees, or surprise rate hikes are less common at credit unions. Transparency is part of their value proposition.

Example: Navy Federal Credit Union provides a business card with no annual fee, competitive APR, and access to exclusive small-business support programs for military-affiliated entrepreneurs.

In short, choosing a credit union business credit card is about more than saving money—it’s about gaining a financial partner who understands and supports your long-term goals.

Fintechzoom.com Crypto News 2025 – Latest Bitcoin, Ethereum & Market Updates

Top Credit Union Business Credit Cards in 2025

Business owners today have more choices than ever when it comes to financing. While big banks dominate advertising, credit unions are quietly offering powerful business credit card products that combine affordability with personalized service. Let’s break down some of the best credit union business credit cards to consider in 2025.

Navy Federal Credit Union Business Credit Cards

Navy Federal is the largest credit union in the U.S., serving military personnel, veterans, and their families. For entrepreneurs with military ties, this is one of the strongest options available.

Key Features:

- No annual fee on most business cards

- APR as low as 13.99% (variable)

- Rewards structure: cash-back on everyday business expenses, including gas and office supplies

- Exclusive programs: access to small business specialists and member-only financial education resources

Example in Action:

Imagine you’re a veteran starting a logistics company. Fuel costs are a huge part of your monthly expenses. By using a Navy Federal business credit card, you could earn cash-back on gas purchases, effectively lowering your operational costs.

PenFed Credit Union Business Credit Cards

Pentagon Federal Credit Union (PenFed) is another major player that serves a broad membership base beyond just military personnel.

Key Features:

- Competitive APR starting at 14.99%

- Rewards tailored for vehicle and travel expenses

- Flexible payment options designed for small businesses with irregular cash flow

- Strong online banking tools and mobile app for business account management

Example in Action:

Suppose you run a small construction company and regularly purchase materials and pay for vehicle maintenance. PenFed’s business card could help you save with extra rewards on those categories, while also keeping costs predictable.

Special Investment Region (SIR): The 2025 Complete Guide for Global Investors

Alliant Credit Union Business Credit Card

Alliant is well known for its consumer credit cards, but its business products are equally competitive.

Key Features:

- Introductory 0% APR period on balance transfers (limited-time offers)

- Low fixed APR after introductory period

- Cash-back rewards on select categories like office supplies and dining

- Dedicated business account management support

Example in Action:

A small digital marketing agency in Chicago could use Alliant’s card to consolidate expenses onto a single card, pay off balances interest-free during the promo period, and then earn rewards on recurring purchases like client dinners and office supplies.

Regional & Local Credit Unions

Smaller regional credit unions often provide extremely competitive rates and a high level of personalization. While they may not have the national footprint of Navy Federal or PenFed, they excel at serving local businesses.

Example:

- A credit union in Maine may offer business cards with APR under 10% for community businesses.

- A local Texas-based credit union might give members special cash-back offers for supporting local vendors.

These localized benefits are unique to credit unions and can give small businesses a real competitive advantage.

TN Bank Business Line of Credit – Rates, Requirements & How to Apply [2025 Guide]

Best Credit Union Business Credit Cards (2025)

| Credit Union | APR (as low as) | Annual Fee | Rewards/Benefits | Best For |

|---|---|---|---|---|

| Navy Federal Credit Union | 13.99% | $0 | Cash-back on gas & office supplies, military benefits | Veterans, military families, logistics businesses |

| PenFed Credit Union | 14.99% | $0–$95 (depending on card) | Extra rewards on travel & vehicle expenses | Construction, travel-heavy businesses |

| Alliant Credit Union | 0% intro APR → 14.49% fixed | $0–$99 | Cash-back on office supplies & dining | Agencies, startups needing balance transfer offers |

| Local/Regional CU | 8–12% | $0–$50 | Personalized rates, community-focused rewards | Local businesses, startups, community-focused owners |

Why These Cards Stand Out

- Cost Savings:

Most credit unions keep fees low and APR competitive, helping businesses reduce financing costs. - Tailored Rewards:

Unlike generic bank rewards, many credit unions customize their programs for small business needs (gas, supplies, travel). - Community Orientation:

Approval is often easier, and decision-makers are accessible compared to large national banks. - Trust Factor:

Credit unions operate under strict NCUA (National Credit Union Administration) guidelines, giving businesses peace of mind that their finances are secure.

Hi Yield (2025) | Savings Accounts, Rates & Benefits Explained

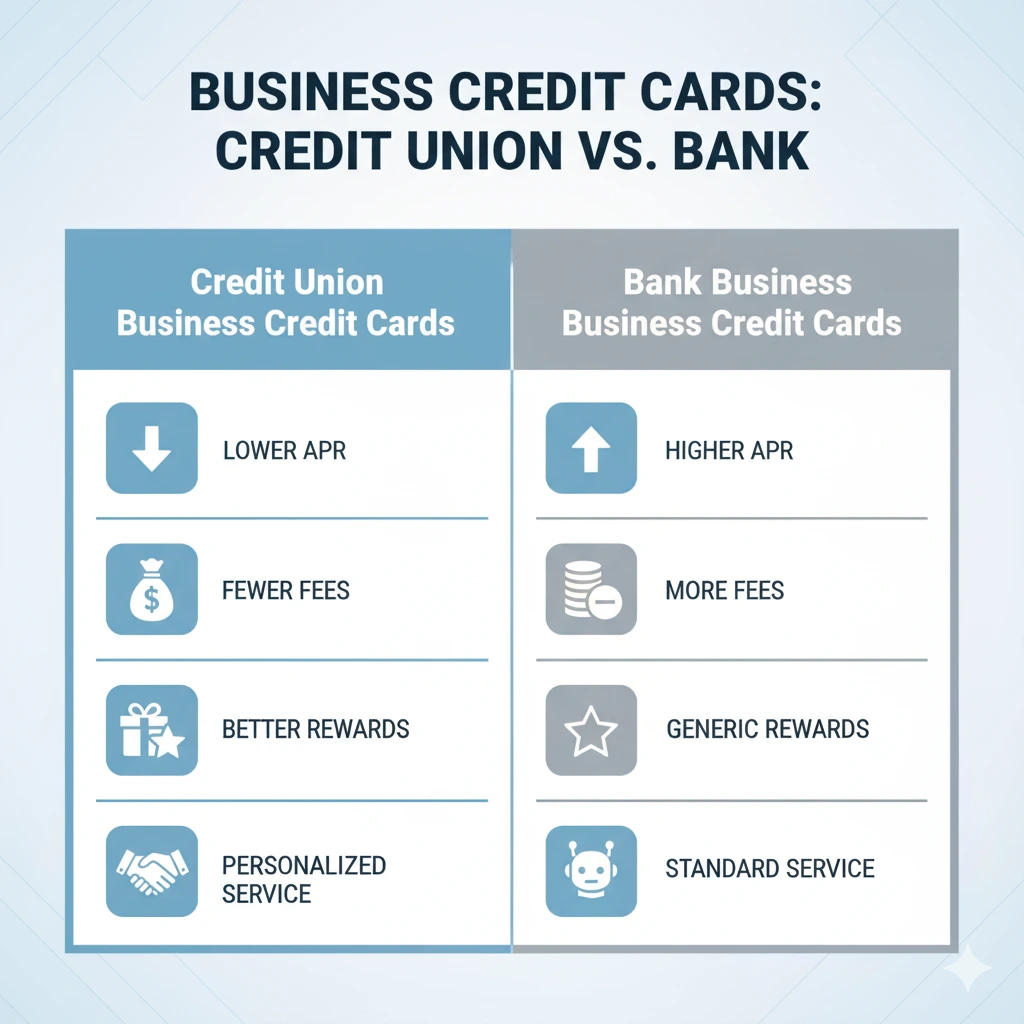

Credit Union Business Credit Cards vs Bank Business Credit Cards

When deciding between a credit union business credit card and one offered by a traditional bank, it’s important to understand the trade-offs.

1. Interest Rates (APR)

- Credit Unions: Typically lower APRs (10–15%).

- Banks: Higher APRs (20–25% common).

👉 For example, a small business carrying a $10,000 balance could save $800–$1,000 annually in interest with a credit union card.

2. Fees

- Credit Unions: Low or no annual fees, minimal penalty charges.

- Banks: Often $95–$500 annual fees, plus balance transfer and foreign transaction charges.

3. Approval Process

- Credit Unions: More flexible, may consider relationship history, local reputation, or collateral.

- Banks: Strictly credit-score and income-driven.

4. Rewards Programs

- Credit Unions: Tailored to small business expenses (gas, supplies, travel).

- Banks: More robust travel and luxury perks but often harder to maximize for small businesses.

5. Relationship

- Credit Unions: Local, personalized, community-based.

- Banks: Global, less personalized, more rigid.

👉 In short: Credit unions are ideal for cost savings and personalized service. Banks may work better for businesses seeking luxury perks or global acceptance.

Christmas Club Account (2025 Guide) – What It Is, Benefits & How It Works

How to Apply for a Credit Union Business Credit Card

Applying for a credit union business credit card is straightforward but slightly different from applying at a bank.

Step 1: Become a Member

- You need to join the credit union first. Membership may be based on location, profession, or community affiliation.

- Example: Navy Federal requires military ties, while PenFed allows broader eligibility.

Step 2: Prepare Your Documents

Most credit unions require:

- Business formation documents (LLC, corporation papers, or sole proprietorship license)

- Employer Identification Number (EIN)

- Business financial statements (income, expenses)

- Personal credit history (since most small business cards require a personal guarantee)

Step 3: Compare Card Options

Check different products offered by your credit union. Some offer rewards, while others focus on low APR.

Step 4: Apply Online or In-Branch

- Online applications usually take 5–10 minutes.

- In-branch applications allow you to discuss your business needs with a representative.

Step 5: Approval & Usage

If approved, you’ll receive your card in 7–10 business days. Responsible usage helps build both business and personal credit history.

Merrimack Valley Credit Union Online Banking & Services (2025 Guide)

Pros & Cons of Credit Union Business Credit Cards

✅ Pros

- Lower APR and fewer fees (ideal for businesses carrying balances).

- Personalized service and flexible approval criteria.

- Tailored rewards programs for small businesses.

- Strong community focus and reinvestment.

- Membership benefits beyond credit cards (business loans, checking, savings).

❌ Cons

- Smaller geographic footprint (limited branches and ATMs).

- Fewer luxury travel perks compared to big banks.

- Limited product variety (may not offer multiple tiers of business cards).

- Some credit unions have strict membership requirements.

Example:

A startup in Ohio might find it easy to get approved for a local CU card, but if they expand operations nationally, they may need a bank card for wider acceptance.

External Resources for Business Credit Cards

Authoritative links improve SEO trust. Consider citing these:

- National Credit Union Administration (NCUA)

- Navy Federal Business Credit Cards

- PenFed Business Credit Cards

- Alliant Credit Union

- Consumer Financial Protection Bureau – Small Business Credit

FAQs About Credit Union Business Credit Cards

Q1. Which credit union has the best business credit card?

👉 Navy Federal and PenFed are often ranked highest due to their nationwide presence, low APRs, and rewards tailored for small businesses.

Q2. Can a new business get a credit union business credit card?

👉 Yes, many credit unions approve startups, especially if you have a strong personal credit score or collateral.

Q3. Do credit union business credit cards report to credit bureaus?

👉 Most do report to major bureaus (Experian, Equifax, TransUnion), which helps build your business and personal credit.

Q4. Are credit union business credit cards better than bank business credit cards?

👉 For affordability and personalized service, yes. For global perks and luxury travel benefits, banks may be better.

Q5. Do credit unions offer rewards like cashback?

👉 Yes, many offer cashback categories like office supplies, fuel, and travel.

Q6. Can I apply online?

👉 Most large credit unions (Navy Federal, PenFed, Alliant) offer full online applications. Smaller CUs may require in-branch applications.

Conclusion

Choosing the right business credit card can make a huge difference in managing cash flow and growing your company. Credit union business credit cards combine affordability, flexibility, and community-focused service—making them one of the best-kept secrets for small and mid-sized businesses in the USA.

Whether you’re a startup looking for your first line of credit, a growing company managing everyday expenses, or a veteran-owned business seeking tailored rewards, credit unions offer solutions that big banks often overlook.

In 2025, business owners should strongly consider credit union cards not only for the financial savings but also for the long-term partnership these institutions provide. By comparing top options like Navy Federal, PenFed, and Alliant, and exploring local credit unions in your area, you can find the perfect card to fit your business goals.

👉 Bottom line: If you want lower costs, personalized support, and a card that works with—not against—your business, a credit union business credit card is one of the smartest moves you can make this year.