Introduction

The question every business is asking in 2025: “How much will cyber insurance cost this year?”

After years of volatile increases, the market is finally stabilizing—but underwriters are stricter than ever. That means your cyber insurance cost 2025 depends less on luck and more on the controls you can prove.

Why this guide matters:

- 💰 Real numbers, not guesswork – see average cyber insurance premiums by business size and industry.

- 📊 Clear pricing factors – understand what actually drives costs up (and how to pull them down).

- 🧮 Simple calculator – estimate your own cyber insurance coverage cost with size + coverage inputs.

- 🔒 Savings strategies – proven ways to reduce cyber insurance cost in 2025 using MFA, Zero Trust, and compliance readiness.

- 📈 Expert forecasts – insights from Marsh, Coalition, IBM, and others on premiums through 2030.

What’s different this year?

- SMBs still face tough pricing if they lack MFA or incident response testing.

- Enterprises are negotiating flat or lower rates—but only with documented controls.

- Average breach costs remain above $4M globally, so insurers aren’t taking chances.

👉 In short, your cyber insurance cost 2025 isn’t fixed—it’s shaped by the security and compliance story you can tell. This guide is your complete playbook: market overview, premium breakdowns, pricing drivers, SMB costs, calculators, reduction strategies, expert insights, FAQs, and a roadmap to smarter insurance buying.

Want the bigger picture on insurer expectations? Read our pillar guide: Cyber Insurance Coverage & Silverfort: 2025 Guide — how MFA, Zero Trust and audit-ready reports influence approvals and premiums. Deep dive: legacy MFA coverage, Zero Trust rollout, and insurer-aligned evidence.

Table of Contents

Average Cyber Insurance Cost in 2025 (By Size & Industry)

When it comes to cyber insurance cost 2025, there’s no single “flat price.” Premiums vary by business size, industry, revenue, and security posture. Still, brokers and carriers publish benchmarks that help us understand the average cost of cyber insurance across the market.

💰 Typical Annual Premiums by Business Size

- Small Businesses (1–100 employees, <$25M revenue):

Most SMBs pay between $1,200–$5,000 per year for a $1M policy. Industry data shows the median premium around $1,740 annually—but lack of MFA, logging, or tested backups can push that figure upward. - Mid-Market Companies (100–1,000 employees, $25M–$1B revenue):

Premiums usually fall between $15,000–$150,000 annually, depending on sector and coverage limits. Businesses that demonstrate strong compliance (NIST, ISO 27001) often sit at the lower end. - Enterprises (1,000+ employees, $1B+ revenue):

Large organizations typically purchase layered programs with higher limits. Annual premiums range from $150,000 to over $1M, depending on claims history and systemic risk exposure.

👉 This tiered view makes it clear that the cyber insurance coverage cost rises exponentially with size, exposure, and regulatory demands.

🏭 Industry-Wise Premium Benchmarks

Different industries face different loss environments, which directly impact premiums:

- Finance & Banking: Highest average premiums due to regulatory pressure and fraud/BEC exposure.

- Healthcare: Elevated costs—sensitive PHI data and downtime risks push prices upward.

- Retail & eCommerce: Mid-level premiums; exposure to card fraud and seasonal cybercrime.

- SaaS & Tech: Wide range; supply chain and vendor risk play a big role.

- Manufacturing: Moderate premiums, but ransomware downtime is a major concern.

Table: Average Premium by Industry & Size (Illustrative)

| Industry | SMB (USD/yr) | Mid-Market (USD/yr) | Enterprise (USD/yr) |

|---|---|---|---|

| Finance | $2,000–$5,000 | $40,000–$200,000 | $300,000–$1M+ |

| Healthcare | $2,000–$6,000 | $50,000–$220,000 | $300,000–$1M+ |

| Retail / eCommerce | $1,500–$4,500 | $25,000–$120,000 | $180,000–$800,000 |

| SaaS / Tech | $1,500–$5,000 | $30,000–$150,000 | $200,000–$900,000 |

| Manufacturing | $1,500–$4,000 | $25,000–$130,000 | $180,000–$850,000 |

Disclaimer: These premium ranges are illustrative benchmarks based on public broker/market data. Actual quotes depend on company size, industry, limits, claims history, and security controls.

🔑 Key Takeaway

The average cost of cyber insurance in 2025 depends less on “what companies your size usually pay” and more on what evidence you can present. Businesses that demonstrate MFA coverage, tested IR plans, and compliance reporting consistently end up below the average premium for their peer group.

Cyber Insurance Cost 2025: Key Pricing Factors

When brokers and underwriters evaluate your company, they aren’t just looking at revenue—they weigh dozens of risk variables. Understanding these cyber insurance pricing factors is critical, because each one can add or subtract thousands of dollars from your premium.

1) Company Size & Annual Revenue

The most obvious factor: larger businesses typically pay more. A 2025 Marsh report shows companies with revenue >$1B routinely spend over $1M annually for layered programs, while SMBs with <$25M revenue often pay under $5,000 (Marsh Cyber Insurance Report 2025). Insurers link scale to potential breach impact—more employees, more systems, and higher probability of large claims.

2) Volume & Sensitivity of Data

A retail SMB processing basic PII will be priced differently than a hospital handling PHI or a bank managing transaction data. IBM’s Cost of a Data Breach 2023 study found healthcare breaches average $10.9M per incident, more than double the cross-industry average (IBM Security, 2023). The more sensitive the data, the higher your cyber insurance cost 2025.

3) Security Posture & Controls

This is where premiums can swing dramatically. Businesses that implement MFA everywhere, deploy Endpoint Detection & Response (EDR), and run regular penetration tests consistently pay less. Coalition reported that insureds without MFA had 5x higher claims frequency in 2023 (Coalition Cyber Claims Report, 2023). Underwriters want proof of controls—not just policies on paper.

4) Claims History

Like auto insurance, prior claims history matters. A company with a history of ransomware payouts or repeated phishing losses is flagged as high risk. Many carriers will surcharge premiums or restrict coverage limits. In some cases, they might exclude ransomware coverage altogether until remediation evidence is provided.

5) Regulatory & Compliance Requirements

Alignment with frameworks like NIST CSF 2.0, ISO 27001, and GDPR plays a growing role. Businesses that can show documented audits and certifications enjoy faster approvals and lower premiums. Insurers increasingly map their questionnaires to these frameworks. For example, NIST’s updated CSF 2.0 now explicitly integrates supply chain security (NIST CSF 2.0, 2024).

6) Industry Risk Profile

Even if two companies have the same revenue and controls, their industry context matters. Finance, healthcare, and SaaS face higher systemic risk and are priced accordingly. Manufacturing and professional services often land at the lower end of premium ranges.

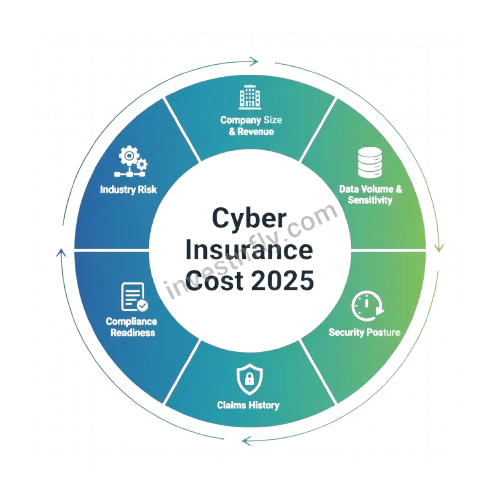

📊 Infographic: The Cyber Insurance Factors Wheel

The six biggest drivers of cyber insurance cost 2025 can be visualized as a wheel, where each slice represents a core pricing factor:

- Company Size & Revenue

- Data Volume & Sensitivity

- Security Posture

- Claims History

- Compliance Readiness

- Industry Risk

Each factor influences how underwriters calculate your premium. Companies that improve their security posture (e.g., MFA, EDR, response testing) and strengthen compliance readiness (e.g., ISO 27001, NIST CSF 2.0) often see the largest premium reductions.

🔑 Key Takeaway

The cyber insurance cost 2025 is not random. It’s the sum of measurable variables. By understanding and improving these cyber insurance pricing factors, businesses can shift from being “high risk” to “preferred insureds,” securing lower premiums and broader coverage.

Cyber Insurance Cost for SMBs

When it comes to the cyber insurance cost for small business, many owners are shocked by how quickly premiums add up. Unlike enterprises that negotiate multi-million-dollar layered policies, SMBs often face higher relative costs because insurers see them as high-risk: limited IT budgets, weaker controls, and limited staff training.

💰 Typical SMB Premium Ranges in 2025

For businesses with fewer than 100 employees and under $25M in revenue, the average cost of cyber insurance in 2025 typically falls between $1,200 and $5,000 annually for a $1M policy. The exact figure depends on security posture:

- A retail shop with basic firewalls and no MFA might get quoted closer to $4,500.

- A consulting firm with MFA and incident response drills might secure coverage around $1,800.

A recent Coalition report found that small businesses accounted for nearly 60% of all cyber claims in 2023, particularly due to ransomware and social engineering (Coalition Cyber Claims Report 2023). This high frequency pushes insurers to price SMBs cautiously.

⚖️ Why SMBs Pay More (Relatively)

- Lower defenses: Many SMBs lack full MFA deployment or EDR solutions.

- Third-party dependency: Heavy reliance on outsourced IT or SaaS creates added exposure.

- Incident impact: Even a small ransomware attack can shut down an SMB for weeks.

- No negotiation leverage: Enterprises can negotiate with multiple insurers; SMBs usually accept off-the-shelf pricing.

This explains why the cyber insurance cost for small business sometimes feels disproportionate compared to enterprise spend.

| Company Type | Employees | Annual Revenue | Typical Premium (USD) | Coverage Limit |

|---|---|---|---|---|

| Small Business (SMB) | 1–100 | <$25M | $1,200 – $5,000 | $1M |

| Mid-Market | 100–1,000 | $25M–$1B | $15,000 – $150,000 | $5M–$10M |

| Enterprise | 1,000+ | $1B+ | $150,000 – $1M+ | $25M–$100M+ |

Disclaimer: Ranges are illustrative 2025 benchmarks. Actual quotes vary by industry, limits/retentions, claims history, and verified security controls.

🔑 Key Takeaway

The cyber insurance cost for small business in 2025 averages around $1,740 per year, but can climb higher without proper security controls. Enterprises may pay millions in absolute terms, but per-dollar-of-revenue, SMBs carry the heavier burden.

For SMBs, the best way to control premiums is to invest early in compliance measures like MFA, employee training, and incident response testing—controls that both protect operations and reduce insurer risk.

Cyber Insurance Cost Calculator (400–500 words)

Premiums often feel like a black box, but most insurers rely on a few core inputs when estimating your coverage price. A cyber insurance cost calculator brings transparency by turning these inputs into an estimated premium range.

🧮 How Calculators Work

A typical cyber insurance cost calculator considers:

- Business size (employees or revenue)

- Coverage limit requested (e.g., $1M, $5M)

- Industry (finance, healthcare, retail, SaaS, etc.)

- Security posture (MFA, incident response, training)

By combining these inputs, calculators provide an estimated annual premium range. While not a formal quote, they help SMBs and enterprises budget and benchmark against peers.

Example Premium Ranges (Illustrative 2025 Data)

- SMB (1–100 employees, $1M coverage): $1,200 – $5,000 per year

- Mid-Market (100–1,000 employees, $5M coverage): $25,000 – $150,000 per year

- Enterprise (1,000+ employees, $25M coverage): $150,000 – $1M+ per year

This demonstrates how premiums scale with both size and requested limits.

Cyber Insurance Cost Calculator (2025)

Cyber Insurance Cost Calculator — 2025 Estimates

Estimate annual premium ranges by business size & coverage limit. Use this as a quick guide — actual quotes vary by industry and security posture.

| Business Size | Typical Coverage Limit | Estimated Annual Premium (2025) |

|---|---|---|

| Micro / Solo Freelancer, single-owner |

$100,000 – $250,000 | $600 – $1,500 |

| Small Business <50 employees |

$250,000 – $500,000 | $1,200 – $2,500 |

| Lower Mid-Size 50–150 employees |

$500,000 – $1,000,000 | $2,500 – $6,000 |

| Mid-Size 150–500 employees |

$1,000,000 – $3,000,000 | $5,000 – $12,000 |

| Large / Enterprise 500+ employees |

$3,000,000 – $10,000,000+ | $20,000 – $60,000+ |

⚠️ Disclaimer

This calculator is for educational purposes only. Actual premiums depend on insurer underwriting, security controls, claims history, and regulatory requirements. Always request a formal quote from licensed brokers.

🔑 Key Takeaway

A cyber insurance cost calculator won’t give you a binding quote, but it does provide clarity. By entering a few details, SMBs and enterprises can benchmark what a realistic cyber insurance coverage cost might be and identify where better security posture could bring premiums down.

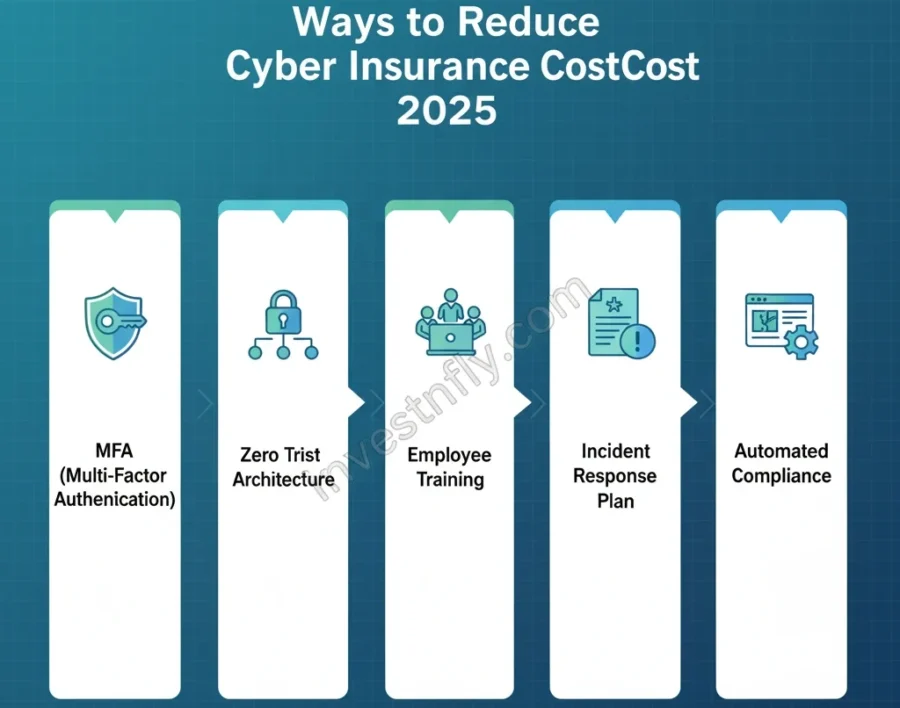

Ways to Reduce Cyber Insurance Costs in 2025

For many businesses, premiums feel like a tax on being digital. But the truth is: insurers reward strong security. By following a few key steps, organizations can significantly reduce cyber insurance cost in 2025 while also improving resilience against attacks.

Step 1: Enforce MFA Everywhere

Insurers now consider MFA (multi-factor authentication) a baseline requirement. Coalition’s 2023 claims report showed organizations without MFA faced 5x higher claim frequency (Coalition, 2023).

- Enforce MFA for all admin accounts, remote access, and cloud logins.

- Extend to third-party vendors accessing critical systems.

Impact: Can reduce premiums by 10–15% because insurers mark you as lower risk.

Step 2: Adopt Zero Trust Principles

Traditional perimeter defense no longer satisfies underwriters. Gartner notes that insurers prefer companies adopting Zero Trust to reduce lateral movement in breaches (Gartner, 2024).

- Segment networks and verify every access request.

- Monitor identity continuously, not just at login.

Impact: Enterprises that document Zero Trust adoption often negotiate premium savings up to 20%.

Step 3: Run Regular Employee Training

Human error is still the top breach vector. IBM’s 2023 breach study found phishing was involved in 16% of breaches (IBM Security, 2023).

- Conduct quarterly phishing simulations.

- Provide bite-sized training modules on suspicious links and password hygiene.

Impact: Demonstrates proactive risk reduction and helps avoid claim disputes later.

Step 4: Build an Incident Response Plan (IRP)

Insurers frequently ask to see your incident response plan before issuing coverage.

- Document roles, escalation procedures, and communication protocols.

- Test quarterly with tabletop exercises.

Impact: Underwriters often cut waiting times for approval when IRPs are validated.

Step 5: Automate Compliance Reporting

Manually collecting logs and screenshots is slow. Tools like SIEM dashboards or solutions like Silverfort compliance cyber insurance automate MFA/identity reports.

- Generate monthly compliance evidence automatically.

- Align reports with frameworks like NIST CSF or ISO 27001.

Impact: Faster renewals, fewer exclusions, and stronger negotiating power.

Mini Case Example: SMB Savings

A 75-employee healthcare SMB implemented MFA, basic Zero Trust segmentation, and automated compliance logs. Their cyber insurance premiums dropped from $4,500 to $2,900 at renewal—a 35% reduction—because the insurer classified them as “low frequency risk.”

🔑 Key Takeaway

Premiums may be rising overall, but organizations that take proactive steps—MFA, Zero Trust, training, IRPs, and automated compliance—are proving they can reduce cyber insurance cost by 15–35%. These are not just insurer checkboxes; they are proven ways to protect both your balance sheet and your business reputation.

Expert Insights 2025

Understanding numbers is one thing, but hearing directly from the experts who shape the market gives a clearer picture of where cyber insurance premiums are headed. Leading insurers, brokers, and analysts agree: costs remain elevated, but businesses that invest in controls can stabilize or even lower their rates.

📢 What Insurers Are Saying

- Coalition (2023 Claims Report):

“Organizations with strong MFA, EDR, and incident response plans consistently see fewer claims and better coverage terms.” (Coalition Cyber Claims Report) - Marsh (2025 Cyber Market Outlook):

“The cyber insurance market is showing signs of stabilization in 2025. While average cost of cyber insurance remains high, improved risk controls and compliance readiness are helping clients achieve more favorable renewals.” (Marsh Cyber Outlook 2025) - IBM (2023 Data Breach Report):

“The global average data breach cost reached $4.45M in 2023, driving insurers to raise rates. Companies that adopt Zero Trust saved on average $1M in breach costs, which directly impacts premiums.” (IBM Security Report 2023)

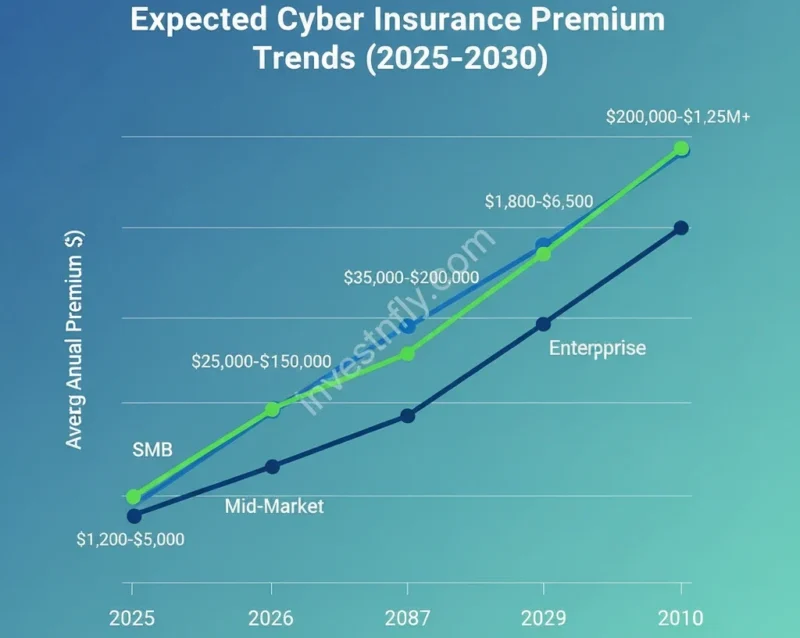

🔮 Premium Predictions: 2025–2030

Experts predict cyber insurance costs will stay volatile but gradually normalize as underwriting models mature and businesses adopt stronger controls.

📊 Table: Expected Premium Trends

| Year | SMB Premium Range ($) | Mid-Market Premium Range ($) | Enterprise Premium Range ($) |

|---|---|---|---|

| 2025 | 1,200 – 5,000 | 25,000 – 150,000 | 150,000 – 1M+ |

| 2026 | 1,300 – 5,200 | 27,000 – 160,000 | 160,000 – 1.05M+ |

| 2027 | 1,400 – 5,500 | 28,000 – 170,000 | 170,000 – 1.1M+ |

| 2028 | 1,500 – 5,700 | 30,000 – 180,000 | 180,000 – 1.15M+ |

| 2029 | 1,600 – 6,000 | 32,000 – 190,000 | 190,000 – 1.2M+ |

| 2030 | 1,800 – 6,500 | 35,000 – 200,000 | 200,000 – 1.25M+ |

Disclaimer: Forecasted premium ranges are illustrative based on industry research and market outlooks. Actual future pricing depends on insurer underwriting models, claims activity, and global cyber risk trends.

🔑 Key Takeaway

The consensus from experts is clear:

- Short-term (2025–2026): Premiums stay high due to breach costs and ransomware threats.

- Medium-term (2027–2028): Stabilization expected as insurers refine risk scoring.

- Long-term (2029–2030): Compliance-driven discounts will dominate, rewarding proactive companies.

In other words, the cyber insurance cost 2025 is a peak point of transition: companies that invest in MFA, Zero Trust, and compliance now will reap the rewards in the years ahead.

FAQs on Cyber Insurance Cost 2025

Q1. What is the average cost of cyber insurance in 2025?

The average cost of cyber insurance in 2025 for small businesses ranges between $1,200 and $5,000 annually for a $1M policy. Mid-market companies can expect $25,000–$150,000, while large enterprises may pay $150,000–$1M+ depending on their coverage limits and risk profile.

Q2. Why are cyber insurance premiums rising in 2025?

Premiums are climbing due to the increasing frequency and severity of cyberattacks, particularly ransomware and supply-chain breaches. According to IBM’s 2023 report, the average global data breach cost hit $4.45M, forcing insurers to adjust pricing upward.

Q3. How much does cyber insurance cost for small business owners?

For SMBs with fewer than 100 employees, the cyber insurance cost for small business is typically $1,200–$5,000 per year for $1M coverage. The exact premium depends on security posture (MFA, EDR, audits), industry, and claims history.

Q4. How accurate are cyber insurance cost calculators?

A cyber insurance cost calculator provides a helpful estimate based on business size, industry, and coverage limits. However, calculators are not binding quotes. Actual premiums depend on detailed underwriting, claims history, and compliance evidence.

Q5. What are the best ways to reduce cyber insurance cost in 2025?

Businesses can reduce cyber insurance cost by enforcing MFA, adopting Zero Trust, training employees, maintaining an incident response plan, and automating compliance reporting. These steps both lower real-world risk and unlock premium discounts of 15–35%.

Managing Cyber Insurance Costs in 2025

The landscape of cyber risk has never been more challenging—and insurers know it. As breaches rise, the cyber insurance cost 2025 reflects both heightened risks and stricter underwriting. But the good news is that companies are not powerless.

By now, you’ve seen how costs vary by business size, industry, and security posture. You’ve also explored the role of calculators, market insights from leading insurers, and proven steps to reduce cyber insurance cost by up to 35%.

The path forward is clear:

- Treat compliance (MFA, Zero Trust, IRP) as non-negotiable essentials, not optional extras.

- Use tools and vendors like Silverfort to simplify reporting and automate compliance.

- Benchmark your costs using calculators and datasets to understand where you stand.

- Learn from expert insights—2025 is a turning point, but proactive businesses will stabilize their premiums faster.

👉 For SMBs and enterprises alike, managing premiums is about more than saving dollars—it’s about securing long-term resilience. If you take steps now, the next five years (2025–2030) could mean consistent protection without unpredictable cost spikes.

🔑 Final Takeaway

Cyber insurance may feel like a cost center, but in reality it’s a business enabler. With compliance readiness, proactive training, and the right partnerships, you not only qualify for coverage faster—you also unlock premium savings that can be reinvested into growth and security.

💡 Start preparing today. Explore solutions like Silverfort and align with frameworks such as NIST CSF 2.0. Because in 2025 and beyond, the smartest investment you can make is in cyber resilience + insurance efficiency.