Plan Your Future with the Dave Ramsey Investment Calculator

Imagine turning just $100 a month into more than $1 million by the time you retire. Sounds unbelievable? That’s exactly the kind of motivation the Dave Ramsey Investment Calculator is built to give you — simple inputs, powerful results.

When it comes to personal finance, few names are as popular as Dave Ramsey. Known for his 7 Baby Steps and debt-free philosophy, Ramsey encourages people to invest consistently and let compound growth do the heavy lifting. His investment calculator is designed to show how even small, steady contributions can snowball into life-changing wealth over time.

On this page, you’ll find a free Ramsey Investment Calculator you can try instantly, along with a complete breakdown of how it works, whether its assumptions are realistic, and how it compares to other popular retirement tools.

Whether you’re a beginner just starting to invest or someone fine-tuning your retirement plan, this guide and calculator will give you a clear picture of where your money could take you.

Start your journey by exploring our detailed guide on investment strategies.

Table of Contents

.

How Does the Dave Ramsey Investment Calculator Work?

The Dave Ramsey Investment Calculator is built to show how small, consistent contributions can grow into long-term wealth. It uses the power of compound interest, where not only your invested money earns returns, but those returns also start generating profits over time.

Enter your details below to see how much your investment could be worth by the time you retire.

Try Our Free Calculator

Dave Ramsey’s Investment Philosophy

When people think of financial freedom, one of the first names that comes to mind is Dave Ramsey. His philosophy is simple: live debt-free, save consistently, and invest for the long term. Unlike many financial influencers who promote quick money strategies, Ramsey focuses on discipline, patience, and steady growth.

Learn more about choosing between mutual funds and ETFs to balance risk and return.

The 7 Baby Steps – Foundation of His Strategy

Dave Ramsey teaches wealth building through his famous 7 Baby Steps:

- Save $1,000 for a starter emergency fund.

- Pay off all debt (except your home) using the debt snowball method.

- Save 3–6 months of expenses in a full emergency fund.

- Invest 15% of household income in retirement accounts.

- Save for children’s college fund.

- Pay off your home early.

- Build wealth and give generously.

The calculator we’ve placed above aligns with Step 4, where consistent investing begins.

The 12% Annual Return Assumption

One of Ramsey’s most debated ideas is his assumption of a 12% average annual return from mutual funds. According to him, history shows that growth stock mutual funds can achieve this over the long run. Critics argue that 7–8% is a more realistic number after adjusting for inflation.

Still, his philosophy isn’t about precision forecasting — it’s about motivation. The high return assumption is designed to inspire people to start investing early and stay consistent.

Why Mutual Funds Over Other Investments?

Ramsey recommends growth stock mutual funds over alternatives like ETFs, individual stocks, or crypto. His reasoning is:

- Diversification → Mutual funds spread risk across many companies.

- Long-term growth → Consistency over decades instead of short-term bets.

- Avoid speculation → He discourages day trading, penny stocks, or cryptocurrencies because of high volatility.

🔹 Comparison Snapshot (Mutual Funds vs Others):

| Investment Type | Dave Ramsey’s View | Risk Level | Expected Return |

|---|---|---|---|

| Growth Mutual Funds | Strongly recommended | Moderate | 10–12% (claimed) |

| ETFs / Index Funds | Acceptable but not emphasized | Moderate | 7–10% |

| Individual Stocks | Risky, not recommended | High | Variable |

| Crypto / Alternatives | Avoid completely | Very High | Unpredictable |

Pros and Cons of Ramsey’s Investment Philosophy

✅ Pros:

- Easy-to-follow system (great for beginners).

- Focuses on debt-free living before investing.

- Promotes long-term discipline and consistency.

- Strong emphasis on avoiding financial risk and speculation.

❌ Cons:

- 12% return assumption may be overly optimistic.

- Heavy reliance on mutual funds (ignores ETFs/modern diversification).

- Doesn’t account for inflation adjustments in simple calculators.

- Somewhat rigid — not suitable for everyone’s risk tolerance.

Wrap-Up for This Section

Dave Ramsey’s philosophy is less about predicting exact numbers and more about creating habits. His calculator demonstrates the incredible potential of compound growth, even if you assume more conservative returns. For investors who want structure and motivation, his system works — but it’s wise to balance it with modern investment options and realistic expectations.

How Accurate Is the Dave Ramsey Investment Calculator?

The Dave Ramsey Investment Calculator is powerful as a motivational tool — it shows how small, regular investments can become large sums through compound interest. But accuracy depends on the assumptions you feed into it. The most controversial assumption is Ramsey’s typical 12% annual return from growth-stock mutual funds. That number is optimistic compared with long-term historical averages after inflation, and real-world returns vary widely depending on market cycles, fees, and asset allocation.

Key factors that affect accuracy

- Assumed annual return: A 12% assumption will produce significantly larger final values than a more conservative 6–8% assumption.

- Time horizon: Longer time horizons smooth volatility and make higher average returns more plausible. Short horizons increase uncertainty.

- Inflation: Nominal returns (e.g., 12%) are not inflation-adjusted. Real purchasing power will be lower if you don’t account for inflation.

- Fees & taxes: Mutual fund expense ratios, advisory fees, and taxes on distributions or withdrawals reduce net returns.

- Contribution consistency: Missing months, lump-sum changes, or irregular investing change outcomes.

- Sequence of returns risk: The order of yearly returns matters more as you near retirement (bad years early/late can hurt).

Example Scenarios (same inputs, different return assumptions)

(Monthly contribution = $500, Start age = 30, Retirement age = 50 — 20 years)

| Scenario | Annual Return (nominal) | Total Contributions | Projected Final Value |

|---|---|---|---|

| Conservative (realistic) | 7% | $120,000 | $247,000 |

| Ramsey Assumption | 12% | $120,000 | $494,000 |

| Aggressive | 15% | $120,000 | $872,000 |

Note: Table shows dramatic differences — 12% vs 7% roughly doubles the final value over 20 years. That’s why the assumed rate is the single biggest driver of “inaccuracy” vs real-world outcomes.

Practical adjustments to improve realism

- Run multiple scenarios: Always show conservative (6–8%), moderate (8–10%), and optimistic (12%+) projections so readers see ranges, not a single optimistic number.

- Show inflation-adjusted (real) returns: Provide an option to subtract an inflation rate (e.g., 2–3%) and display both nominal and real final values.

- Account for fees & taxes: Allow a small annual fee % (0.5%–1.5%) and a tax drag to show net outcomes.

- Display year-by-year snapshot: Let users inspect decade or yearly breakdown so sequence-of-returns and compounding visibility improve trust.

- Explain assumptions clearly: Immediately under the results show the formula and assumptions (annualization method, compounding frequency). Transparency reduces perceived inaccuracy.

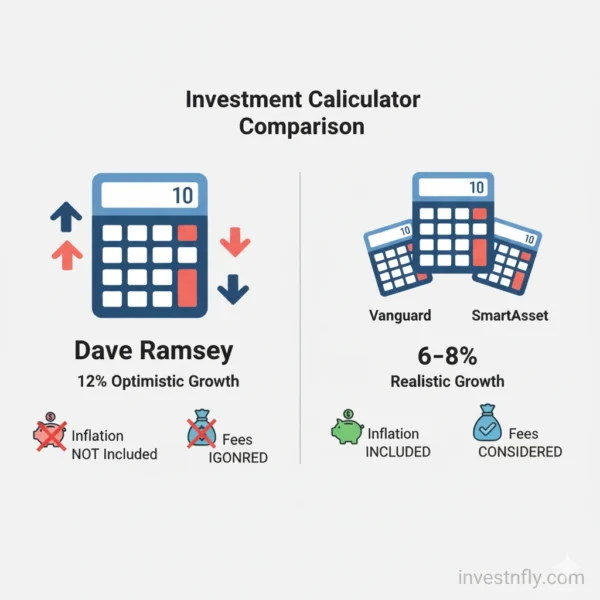

Dave Ramsey Investment Calculator vs Other Retirement Calculators

Most people who search for the Dave Ramsey Investment Calculator also check other tools to compare results. This makes sense — no single calculator can give the perfect prediction. What matters are the assumptions used. While the Ramsey method is highly motivational, many financial planners prefer more conservative estimates.

The Ramsey Investment Calculator is designed for simplicity: just input your age, retirement age, monthly contribution, and expected annual return. By default, Dave Ramsey highlights a 12% return rate from growth stock mutual funds, which creates big final numbers. Other retirement calculators — like those from SmartAsset, Bankrate, Vanguard, or Fidelity — usually assume 6–8% annual growth, include inflation, and sometimes account for taxes or fees.

Key Differences You’ll Notice

- Return Assumptions:

- Ramsey Investment Calculator → assumes 10–12% annual growth (based on long-term stock market history).

- Other calculators → stick to 6–8% returns for realistic financial planning.

- Inflation & Fees:

- Ramsey’s tool does not deduct inflation or management fees by default.

- Other calculators usually subtract 2–3% inflation and show net returns after fund expenses.

- Customization Options:

- Ramsey calculator → keeps inputs simple (monthly savings + return rate).

- Advanced calculators → let you add Social Security, pensions, 401(k)/IRA accounts, tax rates, and healthcare costs.

- Ease of Use:

- Ramsey’s tool → easy for beginners; just 3–4 fields to fill.

- Others → can feel overwhelming for first-time users but provide more detailed insights.

- Motivation vs. Realism:

- Ramsey’s version is built to motivate people to invest early.

- Other tools are built to help people set realistic retirement expectations.

Comparison Table

| Feature / Calculator | Dave Ramsey Investment Calculator | Other Retirement Calculators |

|---|---|---|

| Return Rate Default | 12% (optimistic) | 6–8% (realistic) |

| Inflation Adjustment | ❌ Not Included | ✅ Usually included |

| Fee / Tax Adjustments | ❌ No | ✅ Often available |

| Customization (accounts, income) | Basic only | Advanced options |

| Data Transparency | Limited (simple projection) | Detailed breakdowns |

| Motivation Factor | Very high (big numbers inspire) | Balanced, realistic outlook |

Which One Should You Trust?

If you are new to investing, the Ramsey Investment Calculator is perfect to show you the power of compounding. Seeing how $500 per month can grow into hundreds of thousands — or even millions — is a life-changing motivator.

But if you’re closer to retirement or want a conservative financial plan, you should also run numbers on other calculators. Tools from Vanguard, Fidelity, or Bankrate may give smaller final values, but they include inflation, fees, and risk adjustments that reflect real-world conditions better.

The best approach? Use both. Let the Ramsey calculator inspire you to invest more, but rely on conservative calculators for actual planning.

Takeaway

The Dave Ramsey Investment Calculator shines as a motivational tool, showing the high-end potential of consistent investing. Other retirement calculators balance that optimism with realism. Together, they give you the complete picture: the inspiration to start investing and the caution to plan responsibly.

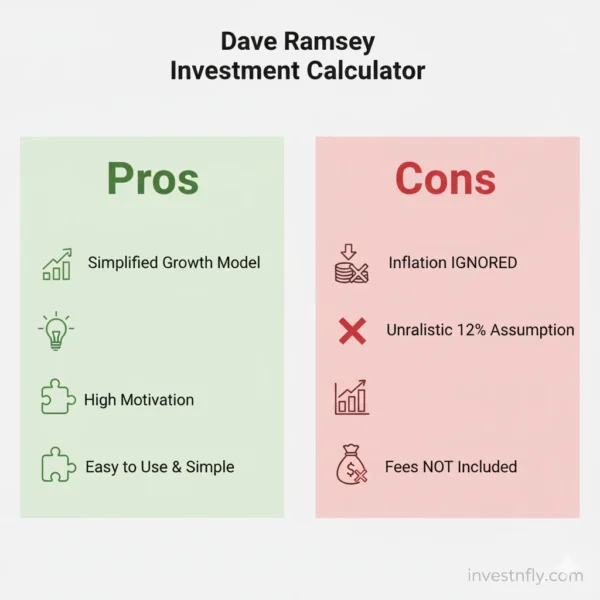

Pros and Cons of the Dave Ramsey Investment Calculator

Like any financial tool, the Dave Ramsey Investment Calculator has its strengths and weaknesses. Knowing both sides helps you use it effectively without building unrealistic expectations.

Pros (Why People Like It)

- Simple to use: Just enter your age, retirement age, monthly contribution, and expected return to get instant results.

- Highly motivational: By assuming 12% annual growth, the calculator shows big future values that inspire consistent investing.

- Demonstrates compounding clearly: It highlights how small monthly contributions snowball into large wealth over decades.

- Perfect for beginners: New investors find it easy to understand and a good first step into retirement planning.

Cons (Where It Falls Short)

- Optimistic returns: The 12% default return is higher than the conservative 6–8% most planners recommend.

- No inflation adjustment: Projections are not reduced for inflation, so actual purchasing power will be lower.

- Excludes fees and taxes: Mutual fund expenses, advisor fees, and taxes are ignored, making results less realistic.

- Limited customization: It doesn’t account for Social Security, pensions, healthcare, or multiple investment accounts.

Takeaway

The Dave Ramsey Investment Calculator is a great motivational tool that encourages people to invest early and consistently. However, it should be paired with more conservative calculators that factor in inflation, fees, and realistic returns for a complete retirement plan.

Pros and Cons of the Dave Ramsey Investment Calculator

| Pros (Strengths) | Cons (Limitations) |

|---|---|

| Very simple and beginner-friendly | Assumes an optimistic 12% annual return |

| Highly motivational — shows big growth potential | No adjustment for inflation, so future value looks larger |

| Demonstrates the power of compound interest clearly | Ignores fees and taxes (makes projections less realistic) |

| Quick way to inspire new investors to start saving | Limited customization (no Social Security, pensions, healthcare, multiple accounts) |

Historical Performance of Stock Market vs Ramsey’s 12% Assumption

The Dave Ramsey Investment Calculator assumes an average 12% annual return from growth stock mutual funds. This assumption is designed to motivate people, but is it realistic compared with actual stock market performance?

Long-Term Market Performance

- Over the last 100 years, the S&P 500 Index (a benchmark for U.S. stocks) has returned about 10% annually on average.

- After adjusting for inflation, the real return drops closer to 7% per year.

- Certain decades — like the 1980s and 1990s — delivered higher returns (sometimes over 12%), but other periods (like the 2000s) saw much lower or even negative averages.

Historical Returns Snapshot

| Time Period | Nominal Annual Return | Inflation-Adjusted (Real) Return |

|---|---|---|

| 1926 – 2023 (long-term) | ~10% | ~7% |

| 1980s – 1990s (strong bull markets) | 12–15% | 9–11% |

| 2000 – 2009 (lost decade) | ~-1% | ~-3% |

| 2010 – 2020 | ~13% | ~11% |

| 2021 – 2023 (volatile years) | ~8% | ~5–6% |

What This Means for the Calculator

- 12% is achievable in certain decades but not guaranteed long-term.

- A more conservative planning rate (6–8%) aligns with most financial planners’ assumptions.

- Using 12% as the only projection can mislead users into expecting unrealistically high retirement savings.

- But as a motivational tool, it’s effective — seeing a million-dollar outcome encourages beginners to start investing.

Practical Advice

- Run multiple scenarios in the Ramsey Investment Calculator:

- Conservative: 6–7% returns

- Moderate: 8–10% returns

- Optimistic: 12%+ returns

- Always consider inflation, fees, and taxes alongside raw growth numbers.

- The calculator is best used for inspiration — pair it with other tools for accurate financial planning.

Alternative Retirement Calculators You Can Try

While the Dave Ramsey Investment Calculator is great for motivation, it’s smart to compare results with other calculators that use different assumptions. This way, you balance inspiration with realism and make more confident financial decisions. Here are some of the most popular alternatives:

1. Vanguard Retirement Nest Egg Calculator

- Focuses on portfolio withdrawal rates and long-term sustainability.

- Allows testing different stock/bond allocations.

- More conservative than the Ramsey calculator.

2. Fidelity Retirement Score

- Creates a personalized retirement readiness score.

- Includes income, expenses, and Social Security.

- Helps you see how close you are to retirement goals.

3. SmartAsset Retirement Calculator

- User-friendly and detailed.

- Includes taxes, inflation, and investment growth.

- Provides customized retirement planning advice.

4. Bankrate Retirement Calculator

- One of the most widely used tools.

- Simple input but includes inflation and expected returns.

- Balanced between ease of use and realistic assumptions.

5. NerdWallet Retirement Calculator

- Great for younger investors starting out.

- Includes contribution tracking, estimated expenses, and savings growth.

- Pairs well with budgeting tools for full financial planning.

Comparison Snapshot

| Calculator | Strengths | Limitations |

|---|---|---|

| Dave Ramsey Investment Calculator | Simple, motivational, big growth projections | No inflation/fees, 12% assumption |

| Vanguard | Conservative, focuses on withdrawals and sustainability | May feel cautious compared to Ramsey |

| Fidelity | Personalized retirement readiness score | More complex inputs needed |

| SmartAsset | Taxes + inflation included, user-friendly | Requires more detailed assumptions |

| Bankrate | Balanced, widely trusted | Fewer customization options |

| NerdWallet | Good for younger investors, tracks expenses | Less detailed than Fidelity or Vanguard |

Takeaway

The Ramsey Investment Calculator is the best tool if you need motivation to start investing and want to see the potential of compounding. But for practical retirement planning, combining it with tools like Vanguard, Fidelity, or SmartAsset gives you a more realistic view. Using two or three calculators side by side is the smartest way to balance inspiration with reality.

How to Use the Ramsey Calculator Effectively

The Dave Ramsey Investment Calculator is built for simplicity, but if you use it wisely, it can do more than just show numbers — it can help you visualize your future, compare scenarios, and stay motivated. Here’s how to make the most out of it:

Step 1 – Enter Your Current Age and Planned Retirement Age

- Your current age sets the starting point, while retirement age sets the horizon.

- Longer horizons = more compounding power.

- Example: someone starting at age 25 vs age 35 could end up with double the money just because of time, even if the monthly contributions are the same.

Step 2 – Add Your Monthly Contribution

- Choose a contribution you can realistically commit to.

- Even $100 per month can grow surprisingly large over decades, while $500 or $1,000 per month can create millionaire-level savings.

- The Ramsey calculator clearly shows how consistent investing beats one-time large contributions.

Step 3 – Choose an Expected Annual Return

- The Ramsey calculator defaults to 12%, which comes from growth-stock mutual fund averages in strong decades.

- To avoid overestimating, also try 6% (conservative) and 8–10% (moderate realistic) returns.

- This way you’ll see both the best-case and realistic-case scenarios side by side.

Step 4 – Calculate and Review the Results

- The calculator will show:

- Total contributions (your real money invested)

- Projected future value (growth + contributions)

- Example: Investing $500/month for 20 years:

- At 7% → ~$247,000

- At 12% → ~$494,000

- At 15% → ~$872,000

This spread demonstrates how sensitive results are to the assumed return rate.

Step 5 – Adjust and Experiment with Scenarios

The Ramsey calculator becomes most useful when you play with numbers:

- Increase your monthly contribution to see how quickly balances rise.

- Change starting age to see how much difference a decade makes.

- Compare short-term (10 years) vs long-term (30 years) horizons.

This hands-on experimenting helps you realize that time and consistency are more powerful than chasing high returns.

Example Scenarios

| Scenario | Starting Age | Monthly Investment | Annual Return | Value at Retirement |

|---|---|---|---|---|

| Early Starter | 25 | $500 | 7% | $247,000 |

| Mid-Life Starter | 35 | $500 | 7% | $122,000 |

| Late Starter | 45 | $500 | 7% | $58,000 |

| Aggressive Investor | 25 | $500 | 12% | $494,000 |

| Max Contribution | 25 | $1,000 | 7% | $494,000 |

👉 Notice how starting 10 years earlier creates almost double the wealth, and doubling your contribution achieves similar results. This is the power of compounding in action.

Practical Tips for Using the Ramsey Calculator

- Run at least three return rates (conservative, moderate, optimistic).

- Include inflation mentally — 12% nominal return translates closer to 9–10% after inflation.

- Add realistic fees (0.5–1% fund expense) to see net returns.

- Revisit annually to update your age, contributions, and goals.

- Pair with other calculators like Vanguard, SmartAsset, or Bankrate to compare.

Key Takeaway

The Ramsey calculator is excellent for motivation and for showing the potential of consistent investing. Use it to test scenarios, play with contributions, and visualize the power of compounding, but always balance it with more conservative calculators for practical retirement planning.

Common Misconceptions & Criticisms of the Dave Ramsey Investment Calculator

The Dave Ramsey Investment Calculator is one of the most searched financial tools, but it’s also one of the most debated. Many people misunderstand what the calculator is meant to do, and critics often point out limitations in its assumptions. Let’s clear up some common misconceptions:

Misconception 1 – “12% Returns Are Guaranteed”

- Reality: The calculator often uses 12% annual growth as the default assumption.

- Critics argue this is too optimistic because long-term stock market averages are closer to 7% after inflation.

- While 12% has occurred during strong decades (like the 1990s), it is not a guaranteed average for all investors.

Misconception 2 – “Inflation Doesn’t Matter”

- Many new investors forget that inflation reduces future purchasing power.

- The calculator shows nominal returns (raw dollar growth) without automatically adjusting for inflation.

- Example: $1,000,000 at retirement may only feel like $600,000 in today’s money if inflation averages 3% per year.

Misconception 3 – “Fees and Taxes Don’t Exist”

- The Ramsey calculator assumes pure compounding growth without subtracting mutual fund fees, advisory fees, or taxes.

- In reality, even a 1% annual fee can reduce final wealth by 20–25% over a 30-year horizon.

- Taxes on capital gains and withdrawals further reduce net value.

Misconception 4 – “The Calculator Predicts the Future Exactly”

- Some users expect the results to be precise forecasts.

- In truth, the calculator is illustrative, showing how money grows under certain assumptions.

- Real-life investing includes market volatility, sequence of returns risk, and unexpected expenses.

Misconception 5 – “Starting Late Doesn’t Make a Difference”

- Critics highlight that many people run the tool late in life and assume they can catch up.

- In reality, the earlier you start, the more powerful compounding becomes.

- Waiting even 10 extra years to start can cut your retirement balance by half.

Key Criticisms Summarized

| Criticism | Why It Matters |

|---|---|

| Overly optimistic 12% assumption | May create unrealistic expectations |

| Ignores inflation | Future value looks larger than real purchasing power |

| No fees or taxes considered | Final results may be overstated |

| Doesn’t model market volatility | Real investing is rarely a straight line |

| Motivational, not predictive | Works as inspiration, not financial planning |

Balanced Perspective

The Ramsey calculator is best understood as a motivational tool, not a planning tool. Its strength is showing the power of compounding in simple terms, especially for beginners. But if you want accuracy for retirement planning, you must combine it with calculators that include inflation, fees, taxes, and realistic market data.

Expert Tips to Use the Dave Ramsey Investment Calculator Wisely

The Dave Ramsey Investment Calculator is useful, but experts recommend combining it with real-world data. Here are some trusted, research-backed tips:

1. Test Multiple Return Rates

- Don’t only rely on 12%. Try 6%, 8%, 10%, and 12%.

- Over the last century, the U.S. stock market delivered about 10% nominal and ~7% real (after inflation) on average, according to Heritage Investments, 2022 (Heritage PDF).

2. Account for Inflation

- Inflation erodes purchasing power. $1,000,000 in 20 years might feel like $600,000 today if inflation averages 3%.

- Investopedia notes that high inflation periods can reduce real stock returns significantly (Investopedia Guide).

- Practical tip: Subtract 2–3% from your calculator results for a realistic value.

3. Don’t Ignore Fees and Taxes

- According to the U.S. Securities and Exchange Commission (SEC), a 1% annual fee can reduce portfolio value by 20–25% over 20 years (SEC Investor Bulletin).

- Ramsey’s calculator skips this — so adjust your expectations by lowering returns ~1% to reflect fees/taxes.

4. Prefer Low-Cost Funds

- Research by SMU Cox School of Business shows most actively managed mutual funds underperform simple index funds after fees (SMU Research).

- Tip: Pair Ramsey’s investing philosophy with low-cost index funds for returns closer to projections.

5. Increase Contributions Gradually

- Even a small annual raise in contributions (2–3%) can multiply final wealth.

- While Ramsey’s calculator doesn’t model this, you can simulate it by manually raising monthly inputs.

6. Revisit the Calculator Regularly

- Use the calculator as a yearly check-up. Update age, contributions, and goals to see if you’re still on track.

Takeaway

Experts suggest that the Ramsey calculator is great for inspiration, but not enough for a full retirement plan. By testing multiple return rates, adjusting for inflation, subtracting fees, and relying on research-backed data (Heritage Investments, Investopedia, SEC, SMU Cox), you’ll combine motivation with accuracy.

Frequently Asked Questions about the Dave Ramsey Investment Calculator

Q1. Is the Dave Ramsey Investment Calculator accurate?

Not exactly. The calculator assumes a 12% annual return from growth stock mutual funds, which is higher than historical averages. Long-term S&P 500 data shows ~10% nominal and ~7% real (after inflation) returns (Heritage Investments, 2022). So while the calculator is great for motivation, it doesn’t reflect inflation, fees, or taxes.

Q2. Why does the Ramsey calculator use 12% returns?

Dave Ramsey bases this on past decades where growth stock mutual funds achieved double-digit returns, especially in the 80s and 90s. However, financial experts like those cited on Investopedia recommend using 6–8% for conservative planning. The 12% figure is mainly for inspiration, not prediction.

Q3. Can I retire a millionaire using the Ramsey calculator?

Yes, if you start early and invest consistently. For example, investing $500/month at 12% for 30 years projects over $1M. But at a realistic 7% return, the outcome is closer to ~$600K. The calculator shows possibilities, but real outcomes depend on inflation, fees, and market volatility.

Q4. How is the Dave Ramsey Investment Calculator different from Vanguard or Fidelity calculators?

The Ramsey calculator is simpler and more motivational. Vanguard, Fidelity, and SmartAsset calculators allow inflation, taxes, and Social Security inputs, giving more realistic estimates. Using both types together balances optimism with practicality.

Q5. Does the Ramsey calculator account for inflation?

No, it does not. All values are shown in future dollars, which can be misleading. For example, $1M in 25 years won’t buy what $1M buys today. Investopedia advises reducing return assumptions by 2–3% to reflect inflation.

Q6. What are the main criticisms of the Ramsey calculator?

Critics argue it:

- Assumes overly optimistic returns (12%)

- Ignores inflation and fees

- Lacks customization options

- Doesn’t reflect market volatility

Despite these, it’s praised for motivating beginners to start investing.

Q7. Can I trust the 12% return assumption?

It’s possible in certain decades, but not guaranteed long-term. According to Heritage Investments, inflation-adjusted U.S. stock returns average closer to 7%. For safety, plan at 6–8% and treat 12% as the optimistic case.

Q8. How often should I use the Ramsey calculator?

Experts suggest revisiting it once a year. Update your contributions, age, and return assumptions. Treat it as a motivational check-up, then cross-check results with conservative calculators like Vanguard or Bankrate.

Q9. Does the Ramsey Investment calculator include taxes?

No. It shows gross investment growth only. The U.S. SEC warns that ignoring fees and taxes can significantly reduce real outcomes. Always consider net-of-tax values when planning retirement.

Q10. What is the best way to use the Ramsey Investment calculator?

Use it for motivation and long-term vision. Run multiple scenarios (6%, 8%, 12%) to see a range of outcomes. Pair it with calculators that adjust for inflation, fees, and taxes for accurate planning.

Should You Rely on the Dave Ramsey Investment Calculator?

The Dave Ramsey Investment Calculator is one of the simplest and most motivational retirement tools available. It does an excellent job of showing how small, consistent investments can grow into life-changing wealth over time. By assuming 12% returns, it paints an inspiring picture of what’s possible if you stay disciplined.

But it’s important to remember: the calculator is not a crystal ball. Real-world investing includes inflation, fees, taxes, and market volatility. Historically, the stock market has delivered closer to 7% inflation-adjusted returns, not 12%. That’s why experts recommend using the Ramsey calculator for inspiration, while relying on more conservative tools (like Vanguard, Fidelity, or SmartAsset calculators) for accurate planning.

The best approach is to use both: let the Ramsey calculator motivate you to start investing now, and let conservative calculators keep your plan realistic. Because at the end of the day, the secret to retiring comfortably isn’t chasing high returns — it’s consistency, time, and discipline.

👉 Try running your own numbers today with the Dave Ramsey Investment Calculator below, then compare with other tools. The earlier you start, the bigger your future will be.