Introduction to Heter Iska Loan

The term “Heter Iska Loan” refers to a unique type of financial arrangement rooted in Jewish law (Halacha). In traditional Jewish practice, charging or paying interest (ribit) is prohibited. To make borrowing and lending possible while respecting these rules, religious authorities developed the concept of Heter Iska — a contract that transforms a loan into a business partnership.

Today, this concept has entered modern banking systems. A few financial institutions in the United States, such as Devon Bank (Chicago) and Cross River Bank (New Jersey), have adopted Heter Iska structures. These loans allow members of the Jewish community, and in some cases non-Jewish borrowers, to access financing that is compliant with kosher financial principles.

This guide will explain everything you need to know about Heter Iska Loans in the USA, including:

- What a Heter Iska financing is and how it works

- Loan requirements and eligibility criteria

- US banks that currently offer these loans

- Step-by-step application process

- Frequently asked questions

👉 Source: Jewish Virtual Library

Traceloans.com Business Loans (2025) – Reviews, Features & Best Alternatives

Table of Contents

What is a Heter Iska Loan?

A Heter Iska loan is not technically a loan in the conventional sense. Instead, it is a business partnership agreement where the borrower receives money and agrees to share potential profits with the lender. Instead of fixed interest payments, the lender’s return is based on a share of the borrower’s earnings.

- Conventional Loan: Borrower repays principal + fixed interest.

- Heter Iska Loan: Borrower repays principal + shares profits (no interest).

👉 Source: Torah.org

📌 Comparison Table – Heter Iska vs Conventional Loan

| Aspect | Conventional Loan | Heter Iska |

|---|---|---|

| Payment Structure | Fixed interest payments | Profit-sharing arrangement |

| Risk for Lender | Low (interest guaranteed) | Shared with borrower |

| Religious Compliance | General finance | Jewish Halacha compliant |

| Example | $10,000 loan → $1,000 interest | $10,000 loan → share of profit |

How Does a Heter Iska Financing Work?

Unlike conventional loans, a Heter Iska is structured as a profit-sharing partnership rather than a debt with fixed interest. In this arrangement, the lender provides capital, and the borrower invests or uses it for business. Instead of paying interest, the borrower agrees to share profits (or potential losses) with the lender.

The contract, known as the “Iska Agreement,” ensures that both parties are legally bound. It is drafted in such a way that it complies with both Jewish Halacha and modern banking laws in the United States.

👉 Source: Devon Bank – Heter Iska

📌 Example Scenario

- A borrower receives $10,000 through a Heter Iska.

- If the borrower’s investment generates a $2,000 profit, a percentage of that profit (say, 20%) goes to the lender.

- If the borrower makes no profit, the lender’s return may be limited or zero, depending on how the agreement is structured.

This differs sharply from a conventional loan, where the lender would receive interest payments regardless of the borrower’s financial outcome.

📊 Table – Loan vs Heter Iska in Practice

| Situation | Conventional Loan Outcome | Heter Iska Outcome |

|---|---|---|

| Borrower earns profit | Pays fixed interest ($1,000) | Shares profit (e.g., $400) |

| Borrower breaks even | Still pays interest | Pays little or no profit share |

| Borrower faces a loss | Still pays interest | Loss may reduce or cancel payment |

Heter Iska Loan Requirements in the USA

To qualify for a Heter Iska loan in the United States, borrowers must meet both standard banking requirements and the additional conditions that make the loan compliant with Jewish Halacha. While exact requirements vary depending on the bank, the general checklist is fairly consistent.

👉 Source: KFI Kosher Finance

✅ General Requirements Checklist

- Valid Identification

- Passport, driver’s license, or state-issued ID.

- Proof of Income

- Pay stubs, tax returns, or business financial statements.

- Loan Purpose

- Documentation of how the funds will be used (home, business, education).

- Iska Agreement

- A signed legal contract drafted under Heter Iska rules.

- Often reviewed or approved by a rabbinical authority.

- Credit & Banking History

- While some lenders are more flexible, most US banks still review creditworthiness.

📊 Table – Conventional vs Heter Iska Loan Requirements

| Requirement | Conventional Loan (USA) | Heter Iska (USA) |

|---|---|---|

| Identification | Yes | Yes |

| Proof of Income | Yes | Yes |

| Credit Check | Always | Sometimes flexible |

| Loan Purpose | Optional | Mandatory (to ensure kosher compliance) |

| Special Contract | Standard loan agreement | Heter Iska Agreement |

| Religious Approval | Not required | Often required (Rabbinical authority) |

📌 Example Note

Suppose you apply for a $50,000 Heter Iska business loan in Chicago:

- You’ll need to provide business financials (like any standard loan).

- The lender will also ensure the agreement is kosher-compliant and signed under Heter Iska principles.

- Unlike conventional loans, your repayment terms will be based on profit-sharing instead of fixed interest.

Can Anyone Get a Heter Iska business loan?

A common question many people ask is whether anyone can apply for a Heter Iska loan in the USA. The answer is: not always.

While Heter Iska loans are designed primarily for the Jewish community, some US banks extend them to non-Jewish borrowers as well. The deciding factor usually depends on the lender’s internal policies and whether they are willing to apply the Iska framework outside of religious necessity.

👉 Source: Cross River Bank – Heter Iska

✅ Who Can Usually Get aHeter Iska business loan?

- Jewish Borrowers

- Most eligible group, since the loan structure directly addresses Halachic restrictions.

- Non-Jewish Borrowers

- May qualify if the bank allows it. Some institutions apply the structure universally, while others restrict it.

- Businesses

- Jewish-owned businesses often prefer Iska-compliant financing. Some banks may extend this option to broader small-business clients.

📌 Key Point Box

Important: Not every US bank recognizes or offers Heter Iska agreements. Always confirm with the lender before applying.

📊 Small Table – Eligibility Overview

| Borrower Type | Eligibility Status | Notes |

|---|---|---|

| Jewish Individual | ✅ Commonly eligible | Meets Halachic requirements |

| Non-Jewish Individual | ⚠️ Case-by-case basis | Depends on lender policy |

| Business (Jewish-owned) | ✅ Often eligible | Widely accepted in communities |

| Business (General) | ⚠️ Limited availability | Rare, depends on bank |

Which Banks Offer Heter Iska business loan in the USA?

In the United States, only a handful of banks provide Heter Iska business loan. These institutions serve niche communities and ensure that their financial products comply with both Jewish Halacha and US banking laws.

👉 Source: Devon Bank – Heter Iska | Cross River Bank – Heter Iska

📊 Table – US Banks Offering Heter Iska Loans

| Bank Name | Location | Loan Types Offered | Notes | Website |

|---|---|---|---|---|

| Devon Bank | Chicago, IL | Mortgages, business loans, personal loans | One of the first US banks to structure Heter Iska financing | Visit Site |

| Cross River Bank | Fort Lee, NJ | Business financing, personal loans | Known for serving Jewish communities in New Jersey and New York | Visit Site |

| Local Synagogue-affiliated Credit Unions | NY, NJ | Community loans | Often smaller, member-based institutions | N/A |

✅ Why Only a Few Banks?

- Limited demand (mostly Jewish borrowers).

- Complexity of creating Halachically compliant agreements.

- Requirement of rabbinical oversight.

Despite this, the demand is strong in specific regions like Chicago, New York, and New Jersey, where Jewish communities are concentrated.

📌 Example Case Study

- Case: A Jewish family in Chicago wants to buy a home.

- Solution: They approach Devon Bank, which structures their mortgage as a Heter Iska agreement.

- Outcome: The family secures financing without violating Halachic restrictions.

Heter Iska Loan vs Conventional Loan

One of the best ways to understand the uniqueness of a Heter Iska business loan is to compare it with a conventional loan. While both provide borrowers with capital, the way repayment is structured — and the underlying purpose — are very different.

👉 Source: BBS Law – Heter Iska Guide

📊 Comparison Table – Heter Iska vs Conventional Loan

| Feature | Heter Iska business loan | Conventional Loan |

|---|---|---|

| Structure | Profit-sharing partnership | Debt with interest |

| Interest | ❌ No fixed interest | ✅ Fixed or variable interest |

| Risk Sharing | Borrower and lender share risks | Risk mostly on borrower |

| Religious Basis | Jewish Halacha compliant | Secular / general finance |

| Legal Contract | Special Iska Agreement | Standard loan contract |

| Availability | Limited to few banks in the USA | Widely available everywhere |

| Use Cases | Home loans, business loans (niche) | All types of loans |

📌 Example Scenario

- Conventional Loan:

Borrower takes $20,000, agrees to pay 5% annual interest = $1,000 per year, regardless of whether the business succeeds or fails. - Heter Iska Loan:

Borrower takes $20,000, invests in a small business. If profit = $5,000, lender may receive a 20% share ($1,000). If no profit, repayment is limited, and lender may bear part of the loss.

👉 This highlights the risk-sharing nature of Heter Iska loans compared to the guaranteed returns of conventional loans.

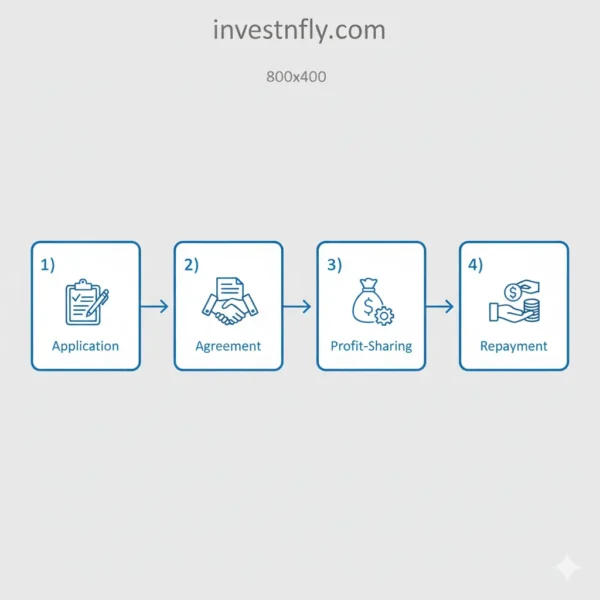

How to Get a Heter Iska Loan in the USA (Step-by-Step Guide)

Applying for a Heter Iska loan in the United States requires both traditional loan paperwork and the special Iska agreement that makes it Halachically compliant. While every bank has slightly different requirements, the general process follows these steps:

👉 Source: ADM Mortgage – Heter Iska

✅ Step-by-Step Process

Step 1: Research Eligible Banks

- Identify which banks offer Heter Iska loans in your area.

- Currently, Devon Bank (Chicago) and Cross River Bank (New Jersey) are the most recognized lenders.

Step 2: Prepare Required Documents

- Provide ID, proof of income, credit history (if required), and details of loan purpose (home, business, or education).

Step 3: Submit Application

- Fill out the bank’s loan application form.

- Indicate that you want the loan structured under a Heter Iska agreement.

Step 4: Sign the Iska Agreement

- This is the critical part.

- The agreement transforms the loan into a business partnership.

- Often reviewed by a rabbinical authority or included as a standard template by the bank.

Step 5: Loan Approval & Fund Disbursement

- Once approved, the bank transfers funds.

- Repayment is tied to profit-sharing instead of fixed interest.

📌 Example Scenario

Imagine you’re applying for a $50,000 small business loan through a Heter Iska arrangement at Devon Bank:

- You provide financial statements showing your business plan.

- The bank structures the loan under an Iska agreement.

- At year-end, your business generates $10,000 profit.

- Instead of paying fixed 6% interest ($3,000), you agree to share a 20% portion of your profit ($2,000) with the lender.

👉 This shows how risk-sharing replaces interest payments in Heter Iska loans.

Pros and Cons of Heter Iska Loans

Like any financial product, Heter Iska loans have both advantages and limitations. Understanding these helps borrowers decide if this structure is the right choice for them.

👉 Source: Patron Law – Heter Iska

✅ Pros of Heter Iska Loans

- Religious Compliance

- Follows Jewish Halacha, avoiding interest (ribit).

- Provides peace of mind to borrowers seeking kosher financing.

- Ethical Financing

- Profit-sharing promotes fairness and discourages exploitative lending.

- Community Acceptance

- Popular within Jewish communities; strengthens trust between borrowers and lenders.

- Flexible Structure

- Payments are tied to actual business outcomes, not fixed interest obligations.

❌ Cons of Heter Iska Loans

- Limited Availability

- Only a few US banks (Devon, Cross River) currently offer it.

- Complex Agreements

- Requires special contracts and sometimes rabbinical oversight.

- Risk for Lenders

- Returns are uncertain since repayment is profit-dependent.

- Not Widely Understood

- Borrowers unfamiliar with Jewish law may find the process confusing.

📊 Example Case

- A borrower takes $100,000 under Heter Iska.

- If the business makes $20,000 profit, lender receives a negotiated share (say $4,000).

- If the business suffers a loss, lender’s share decreases or may be eliminated.

- In contrast, under a conventional loan the borrower would owe interest no matter what.

Pros and Cons of Heter Iska Loans

| Category | Pros (Advantages) | Cons (Limitations) |

|---|---|---|

| Religious Compliance | 100% Halacha-compliant; avoids prohibited interest (ribit) | Only relevant for borrowers seeking kosher finance |

| Financial Structure | Payments tied to profit → no burden during loss years | Uncertain returns for lenders → may discourage large institutions |

| Availability | Offered by banks like Devon (Chicago) and Cross River (NJ) in the USA | Very limited reach; only a handful of US banks provide this option |

| Flexibility | Can be customized for business or mortgage needs | Requires special contracts, sometimes rabbinical supervision |

| Community Impact | Builds trust, especially within Jewish communities | Borrowers outside the community may find access more difficult |

| Risk Sharing | Lender shares business risk with borrower (fairer partnership) | Some lenders may charge higher fees to offset potential risks |

History and Religious Background of Heter Iska

The concept of Heter Iska originates in Jewish history as a response to the biblical prohibition against charging interest (ribit). As Jewish communities engaged in commerce, rabbis created a legal workaround — transforming loans into partnerships.

- Ancient Roots: Based on Talmudic principles that forbid exploitative lending.

- Evolution: Over centuries, rabbinical authorities refined the Iska contract to balance fairness with practicality.

- Modern Application: Today, US banks adapt these contracts to comply with both religious law and American finance regulations.

👉 Source: KFI Kosher Finance

📌 Why This Matters Today

It shows the adaptability of religious law in addressing real-world financial needs.

It bridges religion and modern finance, allowing Jewish borrowers to access mortgages, business loans, and credit without compromising faith.

FAQs — Heter Iska Loans in the USA

1) What is a Heter Iska loan?

This structure is a Halacha-compliant financing arrangement that converts a conventional “interest-bearing loan” into a partnership-style contract. The lender’s return is tied to business profits, not fixed interest.

2) How does a Heter Iska loan work?

Funds are provided under an Iska agreement. The borrower uses the capital for a permitted purpose (e.g., home or business), and the lender earns a pre-agreed share of profits instead of interest. If there is no profit, the return can be reduced or zero, subject to what the contract specifies (e.g., reporting/audit requirements).

3) Who is eligible for a Heter Iska loan?

Primarily Jewish borrowers and businesses seeking Halachically compliant finance. Some US lenders may extend Iska structures to non-Jewish applicants on a case-by-case basis depending on internal policy and product availability.

4) Which US banks offer Heter Iska loans?

Availability is limited. Public examples include Devon Bank (Chicago) and Cross River Bank (New Jersey). In some regions, community lenders or synagogue-affiliated institutions may offer similar structures—always confirm locally.

5) What documents are required?

- Government ID (passport/driver’s license)

- Proof of income (pay stubs/tax returns/business financials)

- Purpose of funds documentation (home purchase, business use, etc.)

- Credit review where applicable

- A signed Heter Iska agreement (often reviewed by a rabbinical authority)

6) Is a Heter Iska loan legal in the USA?

Yes. It’s a contractually recognized arrangement that can comply with US banking and consumer laws when properly structured and disclosed, while remaining consistent with Jewish Halacha.

7) How is it different from a conventional loan?

- No fixed interest; lender’s return is profit-based

- Risk-sharing between borrower and lender (vs. interest due regardless)

- Requires a special Iska contract; availability is more limited than standard loans

Conclusion

Iska financing offer a practical bridge between faith and finance in the U.S., replacing fixed interest with a profit-sharing partnership that aligns with Jewish Halacha. For borrowers who need kosher-compliant funding—and for lenders comfortable sharing business risk—this structure can be a smart alternative to conventional debt. Availability is still limited (mostly regional/community institutions), and the Iska agreement must be drafted with care, so due diligence matters: confirm product types, fees, reporting requirements, and any rabbinic oversight before you sign.

Key takeaways:

- Returns are profit-based, not interest-based.

- Eligibility and terms vary by lender and state.

- Strong fit for Jewish borrowers and businesses; some banks may accept others case-by-case.

- Read the contract carefully—profit definitions, loss handling, and audit rights drive your actual cost.

Next steps:

Compare lenders in your area, gather documents (ID, income, purpose of funds), and speak with both the bank and a qualified rabbinic/ legal advisor. When you’re ready, follow the step-by-step application section above and use the pros/cons and comparison table to decide if Heter Iska is right for you.

For more practical guides and lender updates, visit investnfly.com.