Editorial note: A Heter Iska reframes lending as a profit-sharing partnership consistent with Jewish law (Halacha). Availability varies by lender/state. This page is independent editorial content, not legal advice or an offer of credit.

Who this guide is for

Borrowers who want a clean, lender-friendly workflow to request financing under an Iska agreement—whether for business use (most common) or select real-estate cases. You’ll learn what to say, what to send, and what to double-check before you sign.

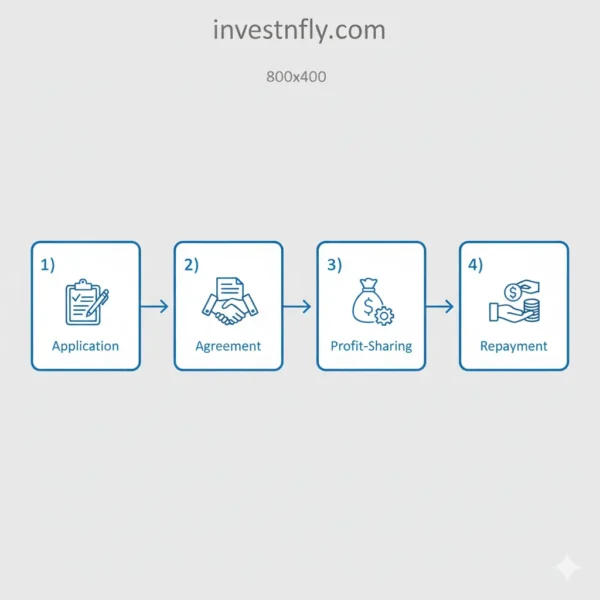

The 6-step application process

1) Shortlist lenders that actually support Iska

- Start with institutions that publicly reference Iska or have a community reputation.

- Confirm state coverage and product type (business, mortgage, personal).

- Pro tip: if consumer mortgages aren’t offered via Iska, ask about owner-occupied commercial where profit tracking is cleaner.

2) Assemble a lender-ready document pack

Treat this like any serious loan: clean PDFs, clear file names, and complete coverage (see full checklist below). Under Iska, you’ll also show how profit can be defined and evidenced.

3) Make first contact the right way

Say you require an Iska-structured facility upfront so you’re routed to the correct team. Ask for a document list and whether they can share a sample Iska agreement or summary (profit definition, reporting, audit, loss/breakeven).

4) Submit the application + documents

Send your pack in one go. In your cover note, state your use of funds, amount, state, and that the deal must be under Heter Iska. Rapid responses to follow-ups can cut days off underwriting.

5) Review the draft Iska agreement

Focus on the five clauses that drive real-world cost and effort:

- Profit definition (EBITDA? net after adjustments?)

- Reporting cadence & format (quarterly/annual; CPA standards?)

- Audit/verification rights (who pays?)

- Breakeven/loss years (is return reduced/zero? carry-forward rules?)

- Fees & early payoff (documentation, late, exit, prepayment)

Ask for plain-English examples in writing before you sign.

6) Close, calendar, comply

After funding, calendar reporting deadlines and payment dates. Keep a simple binder (or folder) with your agreement, statements, and evidence you’ll need at review time.

Documents you’ll need

Personal / W-2 / 1099 applicants

- Government ID, SSN/ITIN as applicable

- Address evidence (recent utility/bank statement)

- Income: 2–3 recent pay stubs or 3–6 months bank evidence; last two years W-2/1099/tax returns

- Bank statements: last 3–6 months

- Purpose-of-funds docs (purchase contract, invoices, dental/medical estimate, etc.)

- Lender’s Iska agreement acknowledgment (later stage)

Business applicants (LLC/Corp/Sole prop)

- Formation docs, EIN, ownership table

- Business tax returns (2 years), YTD P&L and balance sheet (CPA preferred)

- AR/AP aging (if working capital)

- Business bank statements (3–6 months)

- Detailed use-of-funds (quotes, PO, capex list)

- Collateral pack if secured (appraisal, title, insurance/UCC)

- Iska agreement acknowledgment

Packaging tip: name files clearly (2024-Return.pdf, YTD-PnL-2025-08.pdf) and combine small docs to minimize emails.

Sample scenarios (illustrative only)

These examples show how Iska logic can differ from fixed interest. They are not offers.

| Facility | Outcome | Conventional loan (illustrative) | Under a Heter Iska agreement (illustrative) |

|---|---|---|---|

| $50,000 | $10,000 profit | Interest due regardless (e.g., 8% = $4,000) | Lender return is a share of profit (e.g., 20% = $2,000) |

| $50,000 | $0 profit | Interest still due | Return may be $0 per contract; reporting applies |

| $50,000 | $5,000 loss | Interest still due | Return typically $0; loss handling per agreement |

Takeaway: Iska aligns returns with actual performance, but requires evidence (financials, statements) at the cadence set in your agreement.

Pitfalls to avoid

- Assuming “no-doc”: Iska still needs full underwriting.

- Vague use-of-funds: attach quotes, invoices, or purchase agreements.

- Signing without profit clarity: insist on written examples.

- Ignoring reporting: calendar it; ask who pays if audits occur.

- Over-borrowing: pick a plan your cash flow can handle in a bad month.

Call & email scripts

Phone (first call)

“Hi, I’m exploring a Heter Iska-structured [business/mortgage] facility in [state] for [purpose]. Do you currently support Iska for this product and state? If yes, could you send me your document checklist and a summary of the Iska terms (profit definition, reporting/audit, loss handling, early payoff)?”

Email (copy/paste)

Subject: Inquiry — Heter Iska–structured [Business/Mortgage] Facility in [State]

Hi [Name/Team],

I’m seeking a Heter Iska–structured [business/mortgage] facility in [State] for [brief purpose].

Could you please confirm:

1) Current support for Iska in my state + eligible product types,

2) Document checklist and typical timeline,

3) Written summary or sample of the Iska terms (profit definition, reporting/audit, loss/breakeven),

4) Any fees and early payoff conditions?

Thank you,

[Your Name]

[City, State] | [Phone]

Timeline & readiness checklist

| Week | Lender side | Your side |

|---|---|---|

| 1 | Routing to right team | Confirm Iska support; send full doc pack |

| 1–2 | Initial review | Respond to clarifications within 24–48h |

| 2–3 | Draft Iska agreement | Mark-up questions on profit/reporting/audit |

| 3–4 | Final approvals & closing | Arrange collateral items; e-sign; calendar duties |

Readiness checklist:

☑ Clean PDFs, clear file names

☑ Plain-English summary from lender (profit/reporting/audit/loss, fees, prepay)

☑ Side-by-side compare vs conventional option

☑ Post-close reminders for reporting & payments

FAQs — How-to page

1) When should I tell a bank I need Iska?

Immediately—on the first call—so you reach the correct team and template.

2) Can I contact multiple lenders at once?

Yes. Keep a comparison sheet (products/states, fees, profit definition, reporting, early payoff).

3) What if I’m declined?

Ask why (state/policy/size/docs). You may adapt the file or try a lender that supports your use case.

4) Can I see a sample agreement before I apply?

If possible. Even a one-page summary helps evaluate fit before you invest time.

5) Do Iska facilities allow early payoff?

Some do. Confirm prepayment rules and any fees in writing.

6) Who can help me review the agreement?

A CPA (for profit/reporting clarity) and, if needed, legal counsel familiar with banking contracts.

Conclusion

Applying under a Heter Iska agreement is straightforward when you front-load clarity: confirm your lender supports Iska in your state/product, submit a complete file, and get a written summary of profit, reporting, audit rights, and loss/breakeven rules. Compare the Iska path against a conventional loan, choose what fits your faith requirements and cash-flow reality, and calendar your obligations so there are no surprises after funding.