In house financing is when the seller or dealership finances you directly instead of sending you to a bank or credit union. Approval can be faster—and sometimes easier—yet rates and fees are often higher. Always compare with a bank/CU pre-approval before you sign.

Table of Contents

What is In House Financing?

“In house financing” (also called seller financing) means the business that sells you the product also lets you pay over time using its own credit program. You’ll see it in:

- Auto: independent or franchise dealers, including Buy Here, Pay Here (BHPH) lots that approve customers and collect payments directly.

- Furniture & appliances: store-run installment plans or private-label accounts.

- Electronics & other retail: promotional plans (e.g., “no interest if paid in X months”) or fixed-term installments.

The key tradeoff is simple: access and convenience vs total cost. You might qualify when a bank says no—but you’ll often pay more over the life of the agreement. That’s why comparing offers is so important.

How In House Financing Differs From Other Options

It helps to separate three look-alike concepts:

- In House Financing / seller financing

The merchant extends credit itself and services the account (or sets terms and services via an internal affiliate). Payments may be made right at the store/dealer or through the seller’s portal. - Dealer-arranged bank In House Financing (auto)

A dealership collects your application but places the loan with a third-party lender (bank, captive finance, or credit union). The dealer may earn a fee/markup. Day-to-day servicing is by the lender, not the store. - Captive finance

The lender is the manufacturer’s finance arm (e.g., brand-backed auto credit). This is still third-party financing even though it’s tied to a brand, not literally the selling store.

Only (1) is truly “in house.” In daily language, people mix these up—so always ask who the actual creditor is, who services the account, and whether the loan will be reported to credit bureaus.

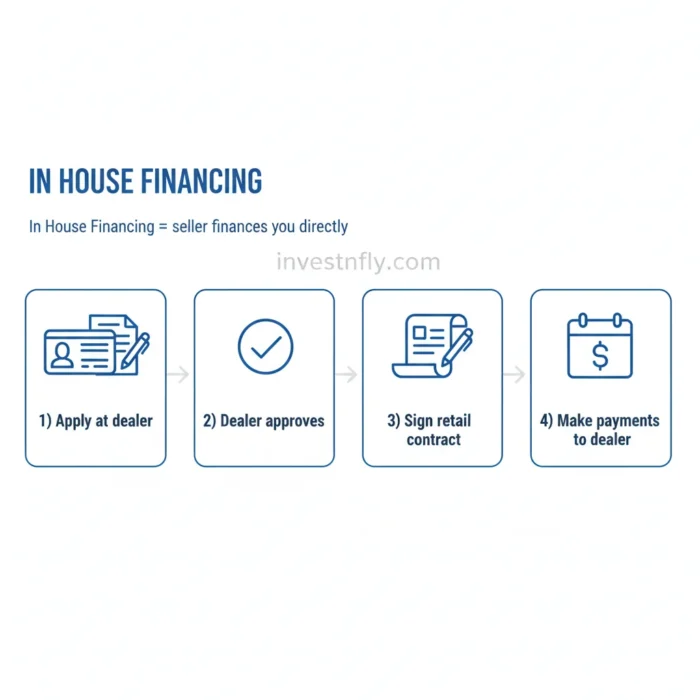

How In House Financing Works (Auto Example)

While every retailer is different, auto is the most common scenario, so we’ll use it to map the flow:

- You apply at the dealership. Provide ID, income proofs, address, and down-payment info.

- The dealer evaluates in-house or BHPH eligibility (or tries outside lenders too). If it’s in house, the credit decision comes from the dealer’s own program.

- You choose a car, sign a retail installment contract, and put down your down payment.

- The title/ELT process (electronic lien/titling in many states) ties the vehicle to the loan until paid off.

- You make payments to the dealer (in person, online, or via auto-debit).

- If you default, in-house lenders—especially BHPH lots—may have strict repossession policies or devices that disable the car if you’re severely delinquent (check your contract carefully).

- When you pay off, the lien is released, and you receive a clear title.

This same idea shows up beyond cars. A furniture store might carry the balance internally; an appliance seller may approve you on the spot with its own installment plan. The paperwork names the creditor—read that line closely.

Buy Now Pay Later Cars (2025): Drive Today, Pay Later – Easy Financing Guide

Who Uses In House Financing and Why

- Thin/no-credit borrowers who struggle to qualify elsewhere but can handle the payments.

- Shoppers who value speed and one-desk convenience more than shopping multiple lenders.

- Buyers with a large down payment who can keep the financed portion small, offsetting some of the cost difference.

It’s not automatically “bad.” It’s just another tool—and like all credit, it’s safe when the math works and risky when it doesn’t.

Pros and Cons at of In House Financing

| Potential Advantages | Potential Drawbacks |

|---|---|

| Faster approvals and one-place shopping | Higher APR/fees than bank/CU in many cases |

| Easier qualification (especially BHPH) | Add-ons can quietly inflate total cost |

| Flexible down payments at some dealers | Strict default remedies (repossession/GPS/ignition-interrupt in some contracts) |

| Convenience (choose + finance in one visit) | May not report to credit bureaus → no score benefit |

Key takeaway: If you can qualify for outside financing, get at least one quote. If in house is still cheaper (all-in), great. If not, use your pre-approval to negotiate or walk.

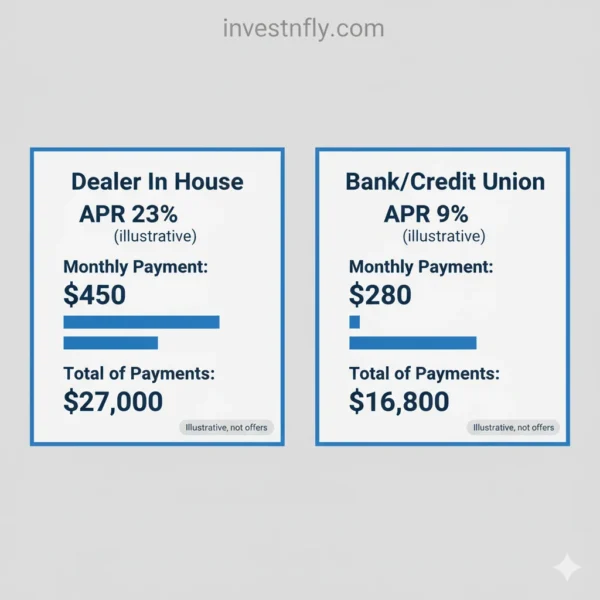

What It Really Costs (Illustrative Examples)

Below are illustrative amortization numbers to show how APR drives your payment and total paid. These are not offers—just math, assuming no taxes/fees/add-ons for simplicity.

36-Month Comparison

| Purchase | APR | Monthly | Total of Payments | Notes |

|---|---|---|---|---|

| $10,000 | 9% | $318 | $11,447 | Typical bank/CU style rate (illustrative) |

| $10,000 | 23% | $387 | $13,935 | In-house/BHPH style example (illustrative) |

| $15,000 | 9% | $477 | $17,171 | |

| $15,000 | 23% | $581 | $20,903 |

48-Month Comparison

| Purchase | APR | Monthly | Total of Payments | Notes |

|---|---|---|---|---|

| $10,000 | 9% | $249 | $11,945 | Longer term lowers payment, raises total interest |

| $10,000 | 23% | $321 | $15,385 | |

| $15,000 | 9% | $373 | $17,906 | |

| $15,000 | 23% | $482 | $23,071 |

What to look at: Don’t just chase the monthly. Focus on the Total of Payments—that’s your true cost of credit.

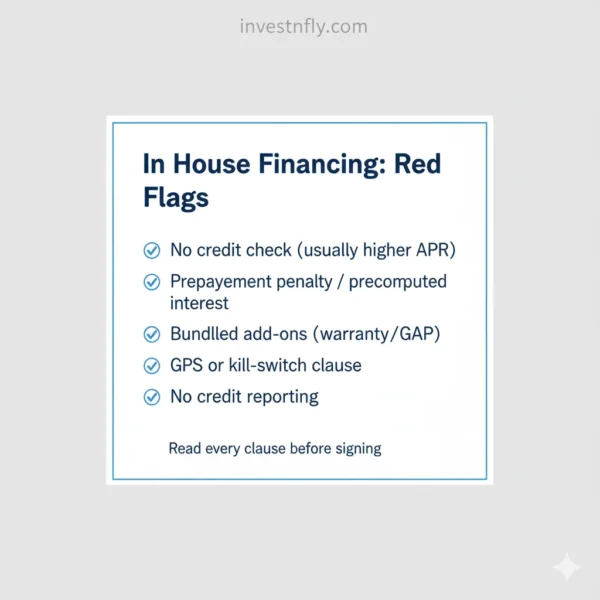

Red Flags to Watch (Read These Twice)

- “No credit check” or “we finance anyone” marketing. It can be real—but the tradeoff is often a much higher APR and strict contract terms.

- Precomputed interest or prepayment penalties. Ask if you can pay off early without fees, and how interest is calculated when you do.

- Bundled add-ons (extended service contracts, GAP, tire/wheel, alarms) slipped in by default. Ask for line-item prices and decline what you don’t need.

- Kill-switch/GPS clauses (auto). Some contracts allow disabling the car for severe delinquency. If present, understand the grace periods and the exact re-enable process.

- No credit reporting. If the lender doesn’t report, your on-time payments may not help your score. Ask explicitly, in writing.

- Pressure to sign fast. You are entitled to read every page of the contract and take a copy. Good businesses won’t rush you.

FTC: dealerships can’t slip in add-ons you didn’t want.

When In House Financing Can Make Sense

- You can handle the payment comfortably, even in a tight month.

- You’ve compared at least one outside offer, and this is the cheapest all-in choice (or the only approval you have).

- You need a reliable car for work and can put down enough to limit risk.

- The contract reports to credit bureaus, so your good behavior helps you later.

- You’ve checked fees, penalties, and add-ons, and you’re okay with them.

When It’s Probably Not the Right Move

- The APR/total cost is much higher than a bank/CU alternative you already qualify for.

- The budget only works if everything goes perfectly; a hiccup would lead to late fees or default.

- The contract includes gotchas (prepayment penalties you can’t live with, aggressive repossession terms).

- The seller refuses to itemize add-ons or won’t let you read the full agreement unhurried.

Documents You’ll Typically Need (Auto)

| Category | What to prepare |

|---|---|

| Identity & address | Government ID, recent utility/bank statement |

| Income | 2–3 pay stubs, W-2/1099, bank statements, or tax return (self-employed) |

| Vehicle | Buyer’s order, VIN, odometer, title/ELT info |

| Insurance | Proof of coverage; GAP if required |

| Payment | Down-payment funds, ACH/debit authorization (if needed) |

Retail store plans ask for similar ID/income proofs, sometimes less.

How to Compare Offers (7 Practical Steps)

- Know your budget. Decide your max monthly payment that leaves room for savings and emergencies.

- Get 1–2 outside quotes first (credit union, bank, or reputable online lender). A pre-approval turns you into a cash-equivalent buyer and gives you leverage.

- Ask the dealer for a written offer that includes APR, term, payment, Total of Payments, all fees, and every add-on line item.

- Calculate the real cost. Use a calculator or the tables above to compare apples-to-apples. The cheapest Total of Payments for the same product/term usually wins.

- Check credit reporting and early payoff. Will they report on-time payments? Can you prepay without fees? How will interest be computed at payoff?

- Read every clause on repossession, late fees, GPS/kill-switch devices (auto), and what happens if you miss a payment.

- Pick the safest, cheapest fit—and keep copies of everything you sign (paper or PDF).

Pro move: Even if you take in house financing now, set a reminder to refinance with a bank/CU in 6–12 months if your credit and market rates improve.

Dealer vs Bank/CU: Side-by-Side (Auto)

| Feature | In House (Dealer/BHPH) | Bank/Credit Union |

|---|---|---|

| Approval speed | Often same day | Same day to a few days |

| Credit tolerance | Wider; may accept thin files | Stricter, especially at better rates |

| APR/fees | Often higher | Often lower |

| Add-ons | Common, sometimes bundled | Available but usually optional and itemized |

| Payment location | At dealer/online | At lender’s portal/app |

| Credit reporting | Ask—varies widely | Typically reports |

| Early payoff | Ask—may have rules | Often allowed, check terms |

Furniture/Electronics Store Example (Non-Auto)

How it looks:

- “No interest if paid in 6/12 months,” or “X months special financing.”

- Store’s private-label account or closed-end installment plan.

- Miss the promo window? Deferred interest may kick in and back-charge interest to day one.

What to do:

- Confirm what happens if you pay late or carry a small balance past the promo period.

- Ask whether the account reports to bureaus (so on-time payments help your score).

- Avoid add-on “protection” you don’t need.

Real-World Scenarios (Illustrative Only)

1) Access matters more than rate

A delivery driver needs a reliable used car this week. Bank denies due to thin credit; the dealer’s in house plan approves with a manageable payment. They accept the higher APR, keep the term modest, and plan to refinance in 9 months after on-time payments.

2) Pre-approval saves money

A buyer gets a CU pre-approval at 9% and visits two dealers. One offers in house at 21% with bundled add-ons. The buyer shows the CU letter; the dealer either matches/places with a third-party lender, or the buyer uses the CU and saves thousands.

3) Store promo traps

A shopper takes a “no interest for 12 months” furniture plan, then pays late in month 13. Deferred interest back-charges from day one. A better move: set automatic payments and pay it off a month early.

Negotiation Script You Can Use

- “Can you show me the APR, term, monthly, and Total of Payments on one page?”

- “Please itemize add-ons like service contracts or GAP so I can choose.”

- “Do you report to credit bureaus? I want my on-time payments to count.”

- “Is there any prepayment penalty or fee to pay off early?”

- “I have a credit union pre-approval at X%. If you can match or beat it all-in, I’ll sign today.”

CFPB’s auto loan guide — great overview of financing options & what to compare.

Say it calmly and be ready to walk. Good businesses will answer directly.

In House Financing FAQs

Is in house financing the same as “buy here, pay here”?

BHPH is a type of in house auto financing where the dealership itself approves you and collects payments. Many dealers also place loans with outside lenders, which is not in-house.

Does in house financing help my credit?

Only if the lender reports. Ask in writing whether they report to the major credit bureaus. If not, your on-time payments may not boost your score.

Are rates always higher than a bank/CU?

Not always, but often higher on average. That’s why pre-approval and side-by-side comparisons are essential.

Can I refinance later?

Usually yes—if your payment history is clean and your credit or market rates improve. Check for prepayment rules first.

What down payment do I need?

It varies by seller, risk, and product. Larger down payments can lower APR, shorten the term, and reduce the chance of owing more than the item is worth.

Is this a good idea for bad credit?

It can be a bridge when the math is safe: affordable payment, clear contract, and a path to refinance or finish fast. If the numbers feel tight, wait, save more down payment, or shop a CU first.

In House Financing Conclusion

In house financing can be the fastest path to a purchase when banks say no—but speed shouldn’t hide the math. If you can, start with a credit-union or bank pre-approval to benchmark cost. When you do consider a dealer/store plan, slow down, read every clause, confirm credit reporting and early-payoff rules, and make sure the Total of Payments still fits your budget. Used carefully, it’s a tool; used blindly, it’s expensive.