Traceloans.com Review 2025 – Introduction

The demand for fast, flexible, and digital-first lending solutions has exploded in the United States over the past few years. Traditional banks, while reliable, are often slow, paperwork-heavy, and restrictive when it comes to approving loans. This gap has given rise to a wide range of online lending platforms that claim to provide quick funding, easier eligibility, and business-friendly repayment terms.

One such name that has recently gained attention is Traceloans.com. If you search on Google, you will find thousands of people looking up phrases like “Is Traceloans.com legit or scam?”, “Traceloans.com business loans”, or “Traceloans.com student loans”. Clearly, borrowers are curious but also cautious about this platform.

The situation is not unique. According to the Consumer Financial Protection Bureau (CFPB), online loan scams and unlicensed lenders have been increasing steadily, especially after the pandemic, as more users turned to digital finance for quick solutions (CFPB – Loan Scams Warning). This is why doing thorough research before engaging with any lender has become essential.

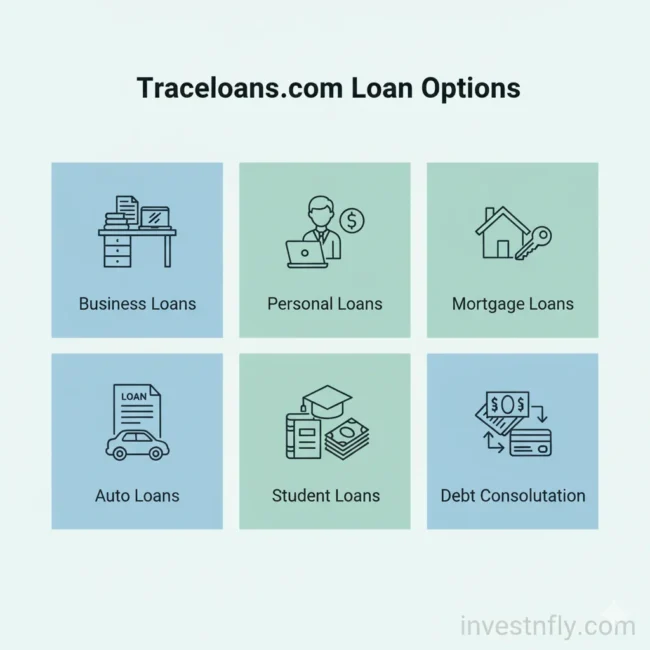

In 2025, Traceloans.com appears to position itself as a one-stop solution for different types of loans:

- Business Loans (for small business growth and payroll management)

- Personal Loans (for emergencies and everyday expenses)

- Mortgage Loans (for home buyers and refinancing)

- Auto Loans (for purchasing vehicles)

- Student Loans (for education financing)

- Debt Consolidation Loans (to merge multiple debts into one)

But here’s the challenge: unlike well-established lenders such as SoFi (sofi.com) or LendingTree (lendingtree.com), Traceloans.com has very little verified information, no clear license disclosures, and multiple suspicious look-alike domains (such as traceloans.net and tracesloans.com). This naturally raises the question: Is Traceloans.com safe for borrowers, or is it just another risky online platform?

In this complete review, we will break down every aspect of Traceloans.com in 2025. You’ll learn about the types of loans it claims to offer, eligibility requirements, pros and cons, credit score considerations, and most importantly, trusted alternatives that are transparent and well-regulated.

By the end of this guide, you will have a clear picture of whether Traceloans.com is worth your attention, and how it compares against legitimate lenders backed by government programs such as SBA loans (sba.gov) or trusted fintech players.

Table of Contents

What is Traceloans.com?

Traceloans.com presents itself as an online lending platform designed to simplify borrowing for individuals and small businesses. Unlike traditional banks that require in-person meetings, strict eligibility criteria, and lengthy approval times, Traceloans.com claims to offer a fully digital loan application process where users can apply online, upload documents, and receive quick decisions.

The platform is not a well-known bank or a government-backed institution. Instead, it falls into the category of fintech-style digital lenders. This category has grown rapidly in the United States, as borrowers increasingly prefer speed and convenience. For instance, TransUnion’s 2024 Consumer Credit Trends Report highlighted that online lenders now make up a large share of unsecured personal loans in the U.S., primarily because of their fast processing times (TransUnion Report).

On its website and across different mentions online, Traceloans.com appears to promote a range of products:

- Business loans to help small businesses cover payroll, marketing, or expansion.

- Personal loans for emergencies and everyday expenses.

- Mortgage loans aimed at home buyers and refinancing.

- Auto loans for vehicle purchases.

- Student loans marketed as education financing solutions.

- Debt consolidation loans to combine multiple debts into one.

At first glance, this variety makes Traceloans.com look like a “one-stop shop” for borrowers. However, the lack of verified company information, licensing details, and official government registrations creates doubt. For example, regulated lenders in the U.S. typically list their NMLS ID (Nationwide Multistate Licensing System) on their websites. Traceloans.com and its variations (such as traceloans.net and tracesloans.com) do not provide this transparency, which is often considered a red flag.

It’s also important to note that multiple domains with similar names exist, some of which are clearly unrelated or spammy. For borrowers, this creates confusion — which site is the real one? In comparison, established fintech platforms like SoFi (sofi.com) or Upstart (upstart.com) maintain a single, consistent domain presence and clear regulatory details.

In summary, Traceloans.com positions itself as a digital-first lending provider, but the absence of trust signals makes it difficult for borrowers to evaluate its legitimacy.Compare such platforms with verified lenders before submitting personal or financial details.

Types of Loans Offered by Traceloans.com

Traceloans.com positions itself as a platform offering different types of loans for businesses, individuals, and students. Instead of specializing in one product, the site promotes multiple categories. This wide coverage attracts attention, but it also raises doubts — because established lenders usually focus on specific loan products.

Below is a breakdown of the major loan types promoted by Traceloans.com in 2025:

1. Traceloans.com Business Loans

Business loans are often the backbone of small business growth. According to the Small Business Administration (SBA), lack of working capital is among the top 3 reasons small businesses struggle (SBA.gov).

Traceloans.com claims to make business funding easier through:

- Online applications with minimal paperwork.

- Quick funding timelines (sometimes within days).

- Flexible loan amounts based on revenue and business profile.

However, since Traceloans.com is not a verified SBA-approved lender, the risk factor is higher. In contrast, traditional SBA-backed loans or fintech players like Bluevine are considered safer options.

We’ve covered Traceloans.com business loans in detail — including application steps, eligibility, and pros/cons — in a separate guide: Traceloans.com Business Loans (2025) – Reviews, Features & Best Alternatives

2. Traceloans.com Personal Loans

For individuals, Traceloans.com promotes personal loans that can be used for emergencies, travel, or medical expenses. Normally, personal loans in the U.S. come with clear APR ranges and terms disclosed by lenders.

Traceloans.com’s personal loan claims include:

- No strict credit requirements (appealing to average/bad credit borrowers).

- Fast approval compared to banks.

- Multiple use cases like debt repayment, daily expenses, or home repairs.

But here again, the absence of transparent APR details and NMLS ID raises questions. Reputed lenders like SoFi or Upstart provide clear interest rate ranges, which makes them more reliable.

3. Traceloans.com Mortgage Loans

Mortgages are among the most heavily regulated loan products in the U.S. Lenders must disclose all costs, from origination fees to interest rates.

Traceloans.com claims to offer:

- Home purchase financing.

- Refinancing options.

Yet, there is no verified information about partnerships with government bodies like Fannie Mae or Freddie Mac. Borrowers should be careful — mortgage scams are common, as highlighted by the Federal Trade Commission (FTC) (FTC Mortgage Scams).

4. Traceloans.com Auto Loans

Auto loans are popular in the U.S., with credit unions and banks dominating the market. Traceloans.com markets itself as an easy option for car buyers who want quick approvals.

Key points it promotes:

- Fast approval for car purchases.

- Options for new and used vehicles.

However, official lenders like Capital One Auto Finance and local credit unions offer detailed, transparent auto loan programs — something Traceloans.com lacks.

5. Traceloans.com Student Loans

Student loans are a sensitive area because of high debt burdens in the U.S. A genuine lender normally provides interest subsidies, deferment, or refinancing support.

Traceloans.com claims to support education funding but does not list:

- Interest rate details.

- Federal loan partnership (like FAFSA).

- Repayment grace periods.

In comparison, trusted student loan providers like Discover Student Loans and federal programs at Studentaid.gov are safer choices.

6. Traceloans.com Debt Consolidation Loans

Debt consolidation is one of the most searched Traceloans.com terms in 2025. Borrowers look for platforms that merge multiple debts into a single monthly payment.

Traceloans.com advertises this service, but again, lacks verified details on:

- Actual APRs.

- Whether it reports to credit bureaus.

- Transparent repayment schedules.

Trusted alternatives include LendingTree (lendingtree.com) and nonprofit credit counseling agencies.

Traceloans.com & Bad Credit Loans

One of the most searched queries connected to Traceloans.com is bad credit loans. Borrowers across the United States often face difficulties when their FICO credit score is below 600. Traditional banks and credit unions usually set strict minimum requirements, leaving millions of people without access to funding. According to Experian’s 2024 Consumer Credit Review, around 16% of Americans have credit scores under 580, which is classified as “poor” credit (Experian). This is the group most actively searching for solutions like “Traceloans.com bad credit loans”.

Traceloans.com markets itself as a platform where poor credit is “not a big problem.” Its promotional claims suggest faster approvals, flexible repayment options, and eligibility even for borrowers with low or no credit history. For people who have been rejected multiple times by banks, such promises sound attractive. But this is also where the risk factor begins.

Why Borrowers with Poor Credit Look to Traceloans.com

When someone has bad credit, they typically encounter:

- Loan rejections from mainstream banks.

- Very high APR offers from payday lenders.

- Difficulty building trust with traditional financial institutions.

Traceloans.com fills this gap by highlighting:

- Quick approval timelines (sometimes within 24–48 hours).

- Minimal paperwork (applications fully online).

- “Bad credit welcome” messaging.

This type of marketing creates hope for borrowers in difficult financial situations. A single search for “Traceloans.com bad credit loans review” shows that many users are curious whether the platform is genuine or just another risky option.

The Risks of Traceloans.com Bad Credit Loans

While fast approval and “no strict credit checks” may sound helpful, they often come with hidden costs. Traceloans.com and its related domains (like traceloans.net and tracesloans.com) do not display:

- Verified APR ranges.

- Clear repayment schedules.

- NMLS licensing details (which are mandatory for U.S. lenders).

The Federal Trade Commission (FTC) warns that unregulated online lenders often target bad credit borrowers with predatory interest rates or hidden fees (FTC Loan Scams). Without verified information, there is a risk that borrowers could end up paying far more than expected.

Common risks reported with platforms like Traceloans.com include:

- Higher-than-average interest rates (sometimes double what banks charge).

- Hidden origination or processing fees.

- Short repayment terms that cause cash flow stress.

- No guarantee that payments are reported to credit bureaus, which means your credit score might not even improve.

In addition, the presence of multiple look-alike domains creates confusion. Borrowers may not know which website is authentic, which increases the possibility of phishing or fraud.

Safer Alternatives for Borrowers with Bad Credit

Borrowers with poor credit do have safer and regulated options that can help them access funds without risking scams. Some of the best alternatives include:

- Credit Unions – Local, member-owned institutions often provide small-dollar loans at lower rates. Because they are nonprofit, their focus is on supporting members, not maximizing profits.

- Online Lenders with Transparent Licenses – Companies like Upstart use AI-based lending models and openly disclose APR ranges. These are licensed and regulated, unlike Traceloans.com.

- Lending Marketplaces – Platforms like LendingTree (lendingtree.com) allow borrowers to compare multiple lenders, giving more choice and transparency.

- SBA Microloans – The U.S. Small Business Administration (SBA) provides microloans for entrepreneurs with limited credit history (SBA.gov). While slower, these loans are safe and government-backed.

- Credit-Building Products – Instead of rushing into risky loans, borrowers can consider secured credit cards, credit-builder loans from community banks, or programs recommended by the Consumer Financial Protection Bureau (CFPB) (CFPB Guide).

By comparing these regulated options, borrowers avoid the hidden traps that platforms like Traceloans.com may present.

Should You Trust Traceloans.com for Bad Credit?

The short answer is: caution is needed. While Traceloans.com promotes itself as a quick solution for people with poor credit, the lack of transparency makes it a risky choice. Legitimate lenders openly display interest rates, repayment terms, and licensing information — none of which are clearly available on Traceloans.com.

For bad credit borrowers, this means:

- If you apply, you may face unexpected costs.

- If you skip regulated lenders, you may miss opportunities to rebuild your credit score.

- If you fall into hidden fees, it could worsen your financial situation.

Conclusion on Bad Credit Loans

In 2025, Traceloans.com bad credit loans remain a highly searched term because many borrowers are desperate for easier funding options. While the platform claims to help those with poor credit, its lack of transparency and absence of regulatory signals are major red flags.

Instead of risking your financial stability with unverified lenders, explore safer alternatives such as credit unions, SBA-backed loans, or trusted fintech platforms like Upstart and LendingTree. These options may take more time, but they offer long-term benefits — including credit score improvement and borrower protection.

Bottom line: Borrowers should approach Traceloans.com bad credit loans with caution and always compare with regulated, transparent lenders before making a decision.

Traceloans.com & Credit Score Impact

Traceloans.com Credit Score Impact – 2025 Review

Whenever borrowers search for loan providers online, one of the most common questions is: “How will this affect my credit score?” With Traceloans.com loans, this concern becomes even more important. Since the platform has limited verified information, understanding the credit score implications is key before applying.

Why Credit Scores Matter in Borrowing

A credit score, usually calculated by FICO or VantageScore, is the three-digit number that lenders use to evaluate borrower risk. According to Experian, scores below 580 are considered poor, while scores above 670 are good (Experian Credit Score Ranges).

Credit scores impact:

- Approval chances – Banks and credit unions set minimum score requirements.

- Interest rates – Lower scores often result in higher APRs.

- Loan limits – Better scores = higher borrowing capacity.

- Future borrowing ability – Every loan decision can either build or hurt your credit history.

For borrowers already in the “bad credit” category, platforms like Traceloans.com appear attractive because of their “no strict credit checks” approach. But the trade-off can be damaging.

How Traceloans.com Claims to Treat Credit Scores

Traceloans.com positions itself as credit-score friendly, targeting those with:

- Poor credit histories.

- Thin credit files (young borrowers).

- Recent rejections from banks.

It suggests that approval is possible without the usual heavy focus on FICO scores. While this may sound helpful, the problem is transparency:

- No details on whether the platform performs a soft pull (pre-approval check) or a hard pull (full credit inquiry).

- No information on whether loans are reported to major credit bureaus like Equifax, Experian, or TransUnion.

- No official data on how repayment behavior is tracked.

If a lender does not report repayments, borrowers lose the opportunity to rebuild their credit history.

The Risks to Credit Scores with Traceloans.com

Borrowers need to consider how Traceloans.com loans could negatively affect their credit:

- Hard Inquiries Without Clarity

- If the platform does a hard credit check during application, your score may drop by a few points.

- Multiple hard checks in a short time can be a red flag for other lenders.

- High APR and Missed Payments

- Borrowers with poor credit are often given high-interest loans.

- If Traceloans.com loans come with hidden fees or short repayment terms, missing payments could quickly damage your score.

- No Credit Reporting

- If repayments are not reported to the bureaus, then even timely payments won’t improve your score.

- This means borrowers take on risk without any long-term benefit.

The Consumer Financial Protection Bureau (CFPB) warns borrowers that many online lenders market to people with poor credit but fail to provide transparency about how credit data is handled (CFPB Guide).

Safer Ways to Protect or Improve Credit Scores

Instead of relying on unclear platforms like Traceloans.com, borrowers can protect or build their credit with these safer strategies:

- Secured Credit Cards – Deposit-based credit cards offered by banks or credit unions. Payments are reported, helping rebuild credit.

- Credit Builder Loans – Offered by community banks and fintech apps like Self or Chime, these are designed to improve credit profiles.

- Personal Loans from Licensed Lenders – Platforms like Upstart (upstart.com) disclose whether they report payments.

- Debt Consolidation via Regulated Marketplaces – Using trusted sites like LendingTree helps ensure payments are tracked.

- Federal Student Loan Programs – For students, federal loans always report repayment, making them safer than unverified online lenders.

By choosing these regulated options, borrowers not only access funds but also improve their credit standing for the future.

Should You Worry About Traceloans.com and Your Credit Score?

The reality is that Traceloans.com credit score impact is uncertain. The lack of transparency around credit checks, bureau reporting, and repayment history means that borrowers could be taking a significant risk.

If the platform does not report to credit bureaus, then borrowers may get funds but gain no long-term credit benefits. If repayment terms are predatory, missed payments could actually make your credit score worse.

In contrast, regulated lenders and credit-building products are far safer choices because they guarantee that repayment data contributes to your credit file.

Conclusion – Credit Score & Traceloans.com

In 2025, Traceloans.com credit score impact remains unclear due to the platform’s lack of verified disclosures. Borrowers with poor credit should be cautious: while the promise of quick approval is tempting, the long-term risk to your credit history may outweigh short-term benefits.

If improving or protecting your credit score is your priority, opt for licensed lenders, credit unions, or government-backed loan programs. These ensure transparency, safer repayment terms, and reliable credit reporting — benefits that Traceloans.com has yet to prove.

Traceloans.com Debt Consolidation Loans

Traceloans.com Debt Consolidation Loans – 2025 Review

Another loan product heavily associated with Traceloans.com in search results is debt consolidation loans. This type of loan is especially popular among U.S. borrowers who are juggling multiple credit cards, payday loans, or medical bills. By combining debts into a single monthly payment, borrowers can simplify their finances and, in some cases, secure a lower interest rate.

According to LendingTree’s 2024 report, debt consolidation searches increased by 18% year-over-year as more Americans looked for ways to manage rising credit card debt (LendingTree). This makes it one of the most important categories to evaluate when reviewing Traceloans.com.

How Traceloans.com Markets Debt Consolidation

Traceloans.com positions itself as a digital-first solution, claiming to:

- Merge multiple debts into one.

- Offer faster approval compared to banks.

- Provide flexible repayment terms.

For borrowers struggling with bad credit, the appeal is obvious. Instead of paying five different bills, Traceloans.com suggests they can handle it all under one loan. The problem, however, is transparency. No verified APR ranges, repayment schedules, or clear terms are provided on the site or associated domains.

The Risks of Using Traceloans.com for Debt Consolidation

While the idea of merging debts is attractive, using unverified lenders like Traceloans.com can make the problem worse. Some of the major risks include:

- High Hidden Costs

- Without disclosed APR, borrowers may face very high interest rates that increase total repayment.

- Short Repayment Cycles

- Instead of lowering financial pressure, short terms may actually cause higher monthly payments.

- No Credit Bureau Reporting

- If the lender does not report repayments to Experian, Equifax, or TransUnion, credit scores won’t improve.

- Multiple Domains Confusion

- Variations like traceloans.net and tracesloans.com create a risk of phishing or fraud.

The Consumer Financial Protection Bureau (CFPB) warns borrowers that many unregulated debt consolidation offers end up being scams or debt traps, especially when they promise quick fixes without clarity (CFPB Debt Consolidation Guide).

Safer Alternatives for Debt Consolidation

Borrowers have safer, regulated, and often cheaper alternatives:

- Credit Unions

- Many offer low-interest debt consolidation loans with transparent repayment terms.

- Lending Marketplaces

- Platforms like LendingTree allow comparison of multiple licensed lenders.

- Nonprofit Credit Counseling Agencies

- Agencies accredited by the National Foundation for Credit Counseling (NFCC) provide structured repayment plans.

- Balance Transfer Credit Cards

- Some banks offer 0% APR introductory offers to consolidate credit card balances.

- SBA Loans for Businesses

- Small businesses can consolidate operational debts with SBA-backed loans.

Compared to Traceloans.com, these options are transparent, regulated, and have strong consumer protections.

Should You Choose Traceloans.com for Debt Consolidation?

The lack of transparency means Traceloans.com is a risky option for debt consolidation in 2025. While the marketing appeals to people struggling with multiple debts, the absence of clear rates, repayment terms, and licensing details makes it difficult to trust.

In contrast, regulated lenders and nonprofit agencies not only disclose all terms but also help improve your credit score by reporting repayments. For borrowers seeking stability, these safer alternatives are far more reliable.

Conclusion – Debt Consolidation & Traceloans.com

In 2025, Traceloans.com debt consolidation loans may sound like a convenient fix for overwhelming debts. However, the risks of hidden costs, unclear terms, and potential scams outweigh the benefits. Borrowers should prioritize transparent, licensed, and nonprofit-backed solutions to consolidate their debts safely.

Bottom line: If you are struggling with multiple debts, avoid shortcuts with unverified lenders like Traceloans.com. Instead, rely on credit unions, LendingTree, or NFCC-accredited agencies to secure a safer and smarter financial future.

Is Traceloans.com Legit or Scam? (2025 Review)

Is Traceloans.com Legit or Scam? A 2025 Review

One of the most common search queries tied to this platform is: “Is Traceloans.com legit or scam?” Borrowers are clearly worried about whether they can trust the site with their personal and financial information. The concern is understandable — online lending has grown rapidly in recent years, but so have online loan scams.

According to the Federal Trade Commission (FTC), consumers in the U.S. lose billions of dollars every year to online financial fraud, much of it tied to fake lending websites (FTC Loan Scams). This makes it critical to evaluate Traceloans.com carefully before making any financial decisions.

Why People Doubt Traceloans.com’s Legitimacy

Several red flags make borrowers suspicious about Traceloans.com:

- Multiple Domains

- Variants like traceloans.net and tracesloans.com exist, creating confusion. Genuine lenders rarely operate with so many lookalike domains.

- Lack of Licensing Information

- Authentic lenders in the U.S. disclose their NMLS ID and licensing details. Traceloans.com does not.

- No Clear Ownership

- The website does not provide corporate ownership details, office addresses, or contact numbers.

- Unverified Reviews Online

- While some review-style blogs promote Traceloans.com, most look like thin content sites with little credibility.

- High-Risk Marketing Language

- Promises like “bad credit no problem” or “fast guaranteed approval” are often associated with predatory lenders.

These points explain why so many people search “Traceloans.com legit or scam” before engaging.

What Legitimate Lenders Usually Provide

To understand the difference, compare Traceloans.com with regulated lenders such as SoFi or Upstart :

- Clear disclosure of interest rates and APR ranges.

- Transparent repayment schedules.

- Secure websites with HTTPS and verified company information.

- Strong customer support with phone/email assistance.

- Reports to major credit bureaus (Equifax, Experian, TransUnion).

Traceloans.com, by contrast, fails to provide these trust signals.

The Risk of Scams in Online Lending

Borrowers should be cautious because online scams often follow predictable patterns:

- Phishing Websites – Fake sites designed to look like lenders but steal data.

- Advance Fee Scams – Asking for upfront payments or “processing fees” before loans are issued.

- Identity Theft – Collecting SSNs, bank account numbers, or tax IDs without offering legitimate loans.

The Consumer Financial Protection Bureau (CFPB) has repeatedly warned against lenders that promise “easy loans” without documentation or that pressure borrowers for upfront fees (CFPB Guide).

If a website like Traceloans.com does not openly publish its loan terms, licensing, and customer support details, it should be treated with extreme caution.

Safer Alternatives to Traceloans.com

Borrowers searching for reliable options should consider:

- Credit Unions – Member-focused and nonprofit, offering lower rates.

- Licensed Fintechs – Platforms like SoFi and Upstart are regulated and transparent.

- Government-Backed Loans – SBA loans for businesses, federal student loans, or FHA mortgages.

- Marketplaces – Websites like LendingTree (lendingtree.com) allow comparisons across trusted lenders.

These alternatives not only provide better protections but also ensure your payments are tracked, which helps build credit history.

Final Verdict – Is Traceloans.com Legit or Scam?

In 2025, there is not enough evidence to call Traceloans.com fully legitimate. The absence of licensing, verified APR details, and transparency puts it closer to the “high-risk” category of lenders. While it may not be outright fraud, the lack of trust signals means borrowers should proceed with extreme caution.

For those asking “Is Traceloans.com legit or scam?”, the safest answer is: treat it as unverified and avoid providing sensitive information until proper transparency is confirmed.

Instead, use trusted platforms like SoFi, LendingTree, or SBA-backed programs for safer, regulated lending solutions.

Comparison Table – Traceloans.com vs Legit Lenders

| Feature / Criteria | Traceloans.com | SoFi | Upstart | LendingTree |

|---|---|---|---|---|

| Licensing / NMLS ID | ❌ Not disclosed | ✅ Yes | ✅ Yes | ✅ Yes |

| APR Transparency | ❌ No clear info | ✅ Ranges published | ✅ Ranges published | ✅ Comparison across lenders |

| Loan Types | Claims multiple (business, auto, student, debt consolidation) | ✅ Personal, student, home loans | ✅ Personal loans, credit-building | ✅ Wide range (mortgage, personal, business) |

| Credit Bureau Reporting | ❓ Unknown | ✅ Yes | ✅ Yes | ✅ Yes (via partner lenders) |

| Customer Support | ❌ Limited / unclear | ✅ 24/7 chat, phone | ✅ Online + phone | ✅ Online + phone |

| Company Transparency | ❌ No verified address or ownership | ✅ Public company | ✅ Licensed fintech | ✅ Established marketplace |

| Reputation / Reviews | ❌ Unverified blogs & mixed mentions | ✅ High Trustpilot ratings | ✅ Transparent reviews | ✅ Thousands of verified reviews |

| Verdict | ⚠️ High Risk / Unverified | ✅ Safe & Legit | ✅ Safe & Legit | ✅ Safe & Legit |

🔹 Disclaimer: The above comparison is based on publicly available information from official lender websites (SoFi, Upstart, LendingTree) and regulatory bodies like the CFPB & FTC (2025). Traceloans.com details are limited due to lack of verified disclosures. Readers are advised to double-check loan terms directly with lenders before applying.

❓ Frequently Asked Questions (FAQ) About Traceloans.com

Q1. Is Traceloans.com a legitimate loan provider?

➡️ At this time, there is no verified evidence that Traceloans.com is a licensed lender. The site does not disclose NMLS ID, APR ranges, or clear ownership details. Borrowers should treat it as high risk until transparency improves.

Q2. Does Traceloans.com offer loans for bad credit?

➡️ The platform claims to approve borrowers with poor credit. However, unlike regulated lenders, there is no clarity on repayment terms, APR, or credit bureau reporting. Safer options include credit unions, LendingTree, and Upstart.

Q3. Will taking a loan from Traceloans.com affect my credit score?

➡️ Unknown. There is no confirmation if repayments are reported to Equifax, Experian, or TransUnion. If they don’t report, your score will not improve. Missed payments, however, could still cause damage.

Q4. What are safer alternatives to Traceloans.com loans?

➡️ Borrowers can explore SoFi, LendingTree, Upstart, credit unions, or SBA-backed loans. These are regulated, transparent, and credit-reporting lenders.

Q5. Can Traceloans.com be a scam?

➡️ Multiple red flags (lookalike domains, lack of licensing, unclear contact info) suggest a possibility of scams. Always check official licensing and never pay upfront fees — a common scam tactic flagged by the FTC.

Conclusion

In 2025, Traceloans.com loans attract attention from borrowers searching for quick approvals and bad credit solutions. However, the lack of transparency on licensing, interest rates, repayment reporting, and ownership details makes it a high-risk choice.

Throughout this guide, we explored Traceloans.com’s offerings in business loans, bad credit loans, debt consolidation, credit score impact, and legitimacy concerns. In each case, one conclusion is clear: borrowers should approach the platform with extreme caution.

Safer, regulated, and verified alternatives such as SoFi, Upstart, LendingTree, SBA loans, and credit unions provide not only funding but also long-term benefits like credit score improvement and borrower protection.

👉 Bottom line: While Traceloans.com may appear tempting, it lacks the trust signals of legitimate lenders. Always prioritize transparency, licensing, and consumer protection when choosing a loan pro